7. Importation Requirements

- 13 Mins to read

- DarkLight

7. Importation Requirements

- 13 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

General Foods

EU

This section provides information on the importation process (shipment, customs, licenses required, and test requirements).

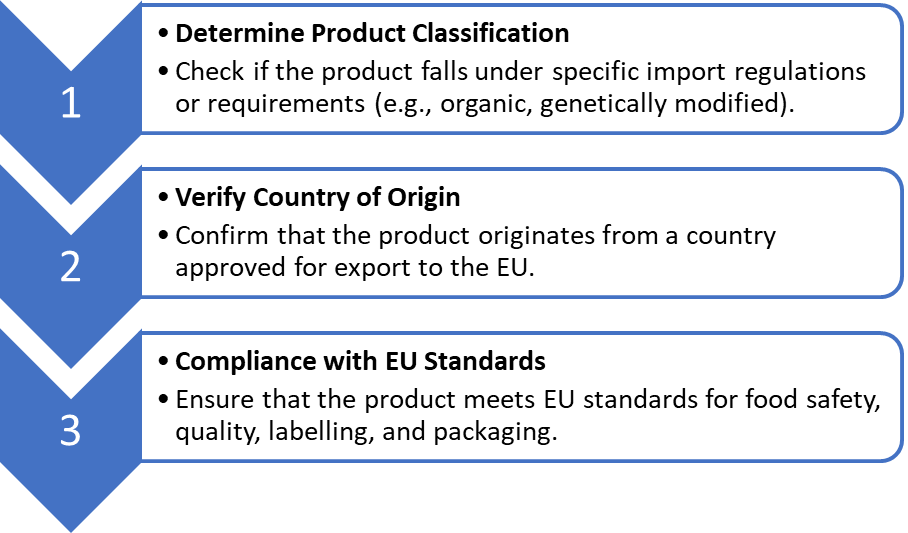

7.1 Shipment Declaration

The importation of food products into the EU is governed by several key regulations, including Regulation (EC) No 178/2002 [1] on general food law, Regulation (EC) No 882/2004 [2] on official controls, and Regulation (EU) 2017/625 [3] on official controls performed to ensure compliance with food law.

Importers are responsible for ensuring that the food products they import comply with EU regulations. Competent authorities in EU member states are responsible for enforcing these regulations and conducting official controls on imported food products.

Before importing food products into the EU, importers must conduct a risk assessment to identify potential hazards associated with the products. This assessment considers factors such as the country of origin, production methods, and previous compliance history.

Importers must ensure that they have the necessary import documentation, including commercial invoices, packing lists, certificates of origin, and health certificates. These documents are required for customs clearance and official controls. The customs declaration can be submitted electronically through the Import Control System (ICS) [4] depending on the country of importation.

The Customs Value Declaration is required for imported goods exceeding EUR 20,000, presented with the Single Administrative Document. Its purpose is to assess the transaction value of goods for customs duties, including all costs until EU entry. Adjustments may be made to the transaction value, such as adding commissions or deducting internal transport costs. Waivers are granted if the value is below EUR 20,000, for non-commercial imports, or if declaration particulars aren't necessary for customs tariff application.

A proof of origin certificates for the country or territory of origin for goods in a consignment. It's declared with the Single Administrative Document (SAD) for customs clearance. There are two types: certificates of non-preferential origin (issued by chambers of commerce) and certificates of preferential origin (issued by the exporting country's customs authorities). Preferential origin certificates allow for reduced or nil duties based on signed agreements. The type of certificate (Form A, EUR MED, or EUR 1) depends on the preferential agreement.

For consignments up to €6,000, invoice declarations can be issued by any exporter in the beneficiary or partner country. However, for consignments beyond €6,000, invoice declarations must be issued only by an approved exporter.

The Bill of Lading (B/L) is a document issued by the shipping company to the shipper, confirming receipt of goods on board and obliging the carrier to deliver them to the consignee. It includes details of the goods, vessel, and destination port. The B/L represents the contract of carriage and transfers ownership of the goods. It can be negotiable and comes in different types, such as clean and unclean bills, which indicate the condition of the goods received.

The road waybill, governed by the CMR Convention, details international road transportation of goods. It allows the consignor control during transit, issued in quadruplicate and signed by consignor and carrier. Copies go to consignor, carrier, and consignee, with one returned to consignor. It's issued per vehicle, not negotiable, and not a document of title.

The air waybill, governed by the Warsaw Convention, is a proof of the transport contract between the consignor and the carrier's company. Issued by the carrier's agent, it can cover multiple shipments and includes three originals and extra copies. Parties involved keep one original each. It's essential at departure/destination airports, for delivery, and possibly for other carriers. The IATA Standard Air Waybill is a common type, embodying standard conditions under the Warsaw Convention.

The rail waybill, regulated by the CIM Convention, is necessary for rail transportation of goods. Issued in five copies by the carrier, the original travels with the goods, the duplicate is kept by the consignor, and the carrier retains the remaining three copies. This document serves as the rail transport contract.

ATA (Admission Temporaire/Temporary Admission) [5] carnets are international customs documents provided by chambers of commerce in many industrialized nations. They enable the temporary importation of goods without customs duties or taxes. ATA carnets cover commercial samples, professional equipment, and items for display or use at trade fairs, exhibitions, and similar events. Additional details are available on the International Chamber of Commerce website [6].

TIR carnets [7] facilitate international goods transportation, particularly when part of the journey is by road, through the TIR procedure established by the 1975 TIR Convention under the UNECE. This procedure requires secure vehicles or containers, an internationally valid guarantee for duties and taxes, and a TIR carnet accompanying the goods, accepted by all transit and destination countries' customs.

Insurance plays a crucial role in goods transportation, covering various risks from handling to rare events like terrorism. Goods transport insurance allows indemnification for covered risks chosen by the policyholder, while carrier's responsibility insurance is subject to specific regulations, offering limited compensation based on weight and value if the carrier is deemed responsible.

For customs clearance, an insurance invoice is required when relevant details aren't included in the commercial invoice, indicating the premium paid for merchandise insurance. Standard transporter responsibility is governed by international conventions.

7.2 Customs Procedure

Importers importing food products into the EU are required to submit customs declarations to the relevant customs authorities. These declarations provide detailed information about the imported goods, including their description, quantity, value, country of origin, and intended use. Importers must ensure that the information provided in the customs declaration is accurate and complete to facilitate smooth customs clearance.

The Harmonized System (HS) is a globally accepted method for categorizing traded goods, developed and maintained by the World Customs Organization (WCO). It uses a hierarchical structure of codes to classify products, enabling over 200 countries to standardize customs tariffs and trade data. Covering a wide range of products, the HS assigns unique codes based on each item's characteristics. This system simplifies customs procedures, aids in collecting trade statistics, and ensures consistency in international trade. Customs authorities use HS codes to determine applicable tariffs, duties, and taxes on imported and exported goods.

Upon submission of the customs declaration, customs authorities assess the applicable customs duties, value-added tax (VAT), and any other taxes or fees payable on the imported food products. Importers are responsible for paying these duties and taxes to customs authorities before the release of the goods.

Customs data requirements are crucial for the exchange and storage of information between customs authorities and economic operators. Electronic data-processing techniques are mandated for this exchange, although other means can be used in exceptional circumstances. The European Union Customs Data Model (EUCDM) defines these data requirements, ensuring compliance with Union and national data protection laws. The EUCDM serves as a model for trans-European customs systems and national customs clearance systems, encompassing various legal provisions outlined in the Union Customs Code (UCC) Delegated and Implementing Acts. These common data requirements are harmonized to ensure consistency across the EU, benefiting economic operators and facilitating regional integration and cooperation between customs administrations. Any changes to these data requirements must be implemented by traders and IT software providers to maintain connectivity with customs systems.

An EORI number, or Economic Operators Registration and Identification number, is a mandatory identifier for customs clearance within the European Union. It uniquely identifies economic operators and others involved in customs operations such as import, export, and transit. The number must be communicated to customs authorities for these operations.

Customs debt refers to the obligation of a person to pay import or export duties as prescribed by customs legislation. This duty arises when goods are placed under a customs procedure, and the customs declaration is accepted. The declarant is responsible for payment, along with any person representing them. Non-compliance with customs legislation can also lead to incurring a customs debt, with various parties potentially liable depending on the circumstances. Customs authorities determine the amount payable and notify the debtor, after which it's entered into accounts. Certain situations exempt customs authorities from notifying debts, particularly for amounts under EUR 10. Repayment or remission of duties may be granted under specific conditions, such as overcharged amounts, defective goods, errors by authorities, or considerations of equity. The threshold value for decisions on non-recovery, repayment, or remission of customs duties was raised to EUR 500,000 as of August 1, 2003. Additional guidelines and decisions by the Commission provide further clarification and procedures regarding customs debt.

Temporary storage refers to the period during which non-Union goods brought into the customs territory of the EU are held under customs supervision until they are placed under a customs procedure or re-exported. These goods are stored in authorized facilities or designated places approved by customs. Typically, temporary storage facilities are operated by importers or storage keepers who provide guarantees against potential customs debts. Customs may authorize the movement of goods between different temporary storage facilities under specific conditions. During temporary storage, goods may only be handled to preserve them, with limited exceptions for examination or sampling with customs permission. Goods must be placed under a customs procedure or re-exported within 90 days of presentation to customs. If this time limit is exceeded, customs authorities may take measures such as confiscation, sale, destruction, or abandonment of the goods at the expense of the declarant.

Pre-Arrival & Pre-Departure Declarations - Regulation 648/2005 [8] amending regulation 2913/92 mandates traders to provide advance information to customs authorities regarding goods entering or leaving the EU's customs territory. This aims to enhance risk analysis and expedite processes upon arrival, benefiting traders. However, implementation depends on defining data elements, time limits, variations, exceptions, and the framework for risk information exchange among Member States. Discussions commenced in July 2005, involving trade federations to ensure sectoral representation. Anticipated timeframes for prior declarations vary, with a 24-hour deadline for sea shipments and shorter deadlines for other modes.

A single authorization is granted by multiple customs administrations within different EU Member States and covers various customs procedures or end-use relief. These include customs warehousing, inward processing, processing under customs control, temporary importation, and outward processing. For instance, a company conducting processing operations in Spain, France, and Italy can obtain a single authorization to cover these activities. Applications must be made using the national form specified in Annex 67 of the Implementing Provisions to the Community Customs Code [8], except for temporary importation, which can be done via a customs declaration or ATA/CPD carnet. The application is submitted to customs authorities based on the location of the applicant's main accounts and where the storage or processing operations occur. If unclear, it's submitted to authorities overseeing the main accounts for customs purposes. Some Member States provide contact details for submitting applications on their websites.

Centralized Clearance (CC) under the Union Customs Code (UCC) allows economic operators to lodge customs declarations at their established customs office for goods presented at another customs office within the EU. This simplification integrates accounting, logistics, and distribution, reducing administrative and transaction costs. Legal basis includes UCC Articles 179, UCC DA Article 149, and UCC IA Articles 229-232, among others. Existing Single Authorization for Simplified Procedures (SASP) remains valid until deployment of the Customs Clearance Infrastructure (CCI) and Automated Entry System (AES). Reassessment of SASP for CC should begin early to ensure full implementation upon system readiness, considering consultation periods and other procedural requirements.

Legal basis for Centralized Clearance:

- Union Customs Code (UCC) Article 179 [9]

- UCC Delegated Act (DA) Article 149 [10]

- UCC Implementing Act (IA) Articles 229-232 [11]

- UCC Transitional Delegated Act (TDA) Articles 18-20 [12]

Online services and databases for customs are shown on the European Commission website under Taxation and Customs Union – Online Services [13].

The Integrated Tariff (TARIC) [14] provides information on all trade policy and tariff measures that apply to specific goods in the EU. It is made up of an 8-digit code of the CN plus 2 extra digits (TARIC subheadings). It ensures the uniform application of these measures across all EU member states and provides clarity for economic operators during import and export processes.

7.3 Manufacturing License

To import food products into the EU, no manufacturing license is needed. However, finding trade partners, possibly through networks like the Enterprise Europe Network [15] or Chambers of Commerce [16], is essential.

Import conditions and duties vary based on the import method, typically requiring establishment in the EU, VAT registration, and locating an EU-based exporter to act on your behalf. Registration with the National Commercial Register via the Chamber of Commerce is necessary. Economic operators within and outside the EU involved in customs activities need an EORI number, obtained from the National Customs Authority, consisting of a two-letter country code and a unique identifier. EORI numbers do not expire but can be invalidated upon request or cessation of business. Validity can be checked through an open interface.

7.4 Test for Importation

There is no specific test needed to support the importation process, and test results will not be asked at the EU border. As presented in Section 7.1 above, relevant attestation and health certificate must be submitted at the BCP.

However, it is the responsibility of the food business operator to ensure due diligence measures are in place and documented in Hazard Analysis and Critical Control Point (HACCP) or food safety management systems, in order to mitigate the risk in food. Please refer to Section 8 - Safety Parameters - for further details.

In addition, provisions for the sampling and analysis of contaminants have been established by various Commission Regulations. These regulations outline the authority procedures for monitoring and controlling the levels of specific contaminants in food products, especially of food products/composite products of animal origin. Foods that present an identified safety risk are listed in the Commission Implementing Regulation 2019/1793 [17]. Article 12 of this Regulation requires the EU Commission to review the lists set out in the Annexes on a regular basis, not exceeding six months.

7.5 Other Notes or Requirements for Importation

The EU general food safety principles for imported products are defined in Regulation (EC) No 178/2002 [1]. Article 11 mandates that 'Food and feed imported into the Community for placing on the market within the Community shall comply with the relevant requirements of food law or conditions recognized by the Community to be at least equivalent thereto or, where a specific agreement exists between the Community and the exporting country, with requirements contained therein.'

Article 19 of this Regulation defines the responsibilities of food importers: 'If a food business operator considers or has reason to believe that a food which it has imported is not in compliance with the food safety requirements, it shall immediately initiate procedures to withdraw the food in question from the market where the food has left the immediate control of that initial food business operator and inform the competent authorities thereof.'

As a result, the imported food products must be produced under at least equivalent standards as all safety parameters presented in Section 8 of this guidebook.

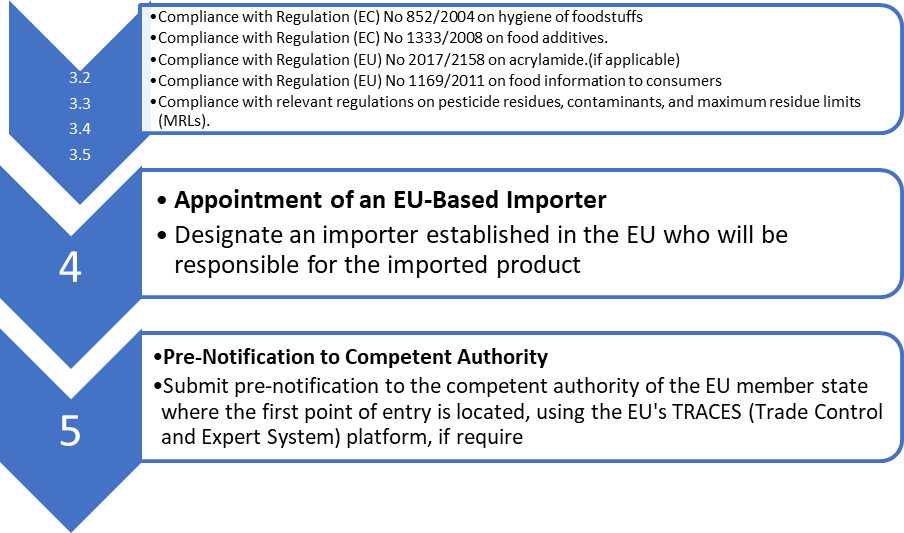

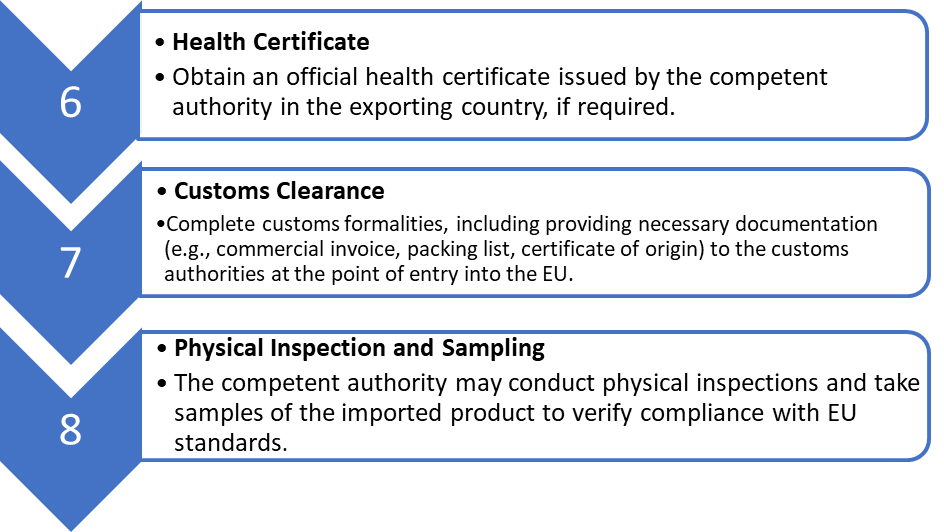

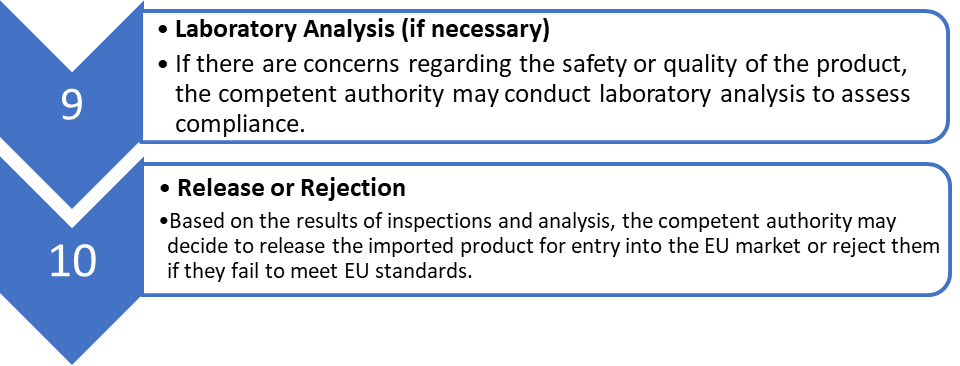

7.6 Overview Flowchart for Importation Process

7.7 References

1. General Food Law Regulation 178/2002

Regulation - 178/2002 - EN - EUR-Lex (europa.eu)

2. Official Controls Regulation (EC) No 882/2004

Regulation (EC) No 882/2004 of the European Parliament and o... (europa.eu)

3. Official controls performed to ensure compliance with food law Regulation 2017/625

Regulation - EU - 2017/625 - EN - EUR-Lex (europa.eu)

4. ICS

Import Control System 2 (ICS2) - European Commission (europa.eu)

5. ATA (Admission Temporaire/Temporary Admission)

ATA Carnet, Chamber International completion guide (chamber-international.com)

6. International Chamber of Commerce

Chamber International, export and import support for business (chamber-international.com)

7. What is a TIR carnet

What is TIR | IRU | World Road Transport Organisation

8. Community Customs Codes Regulation 648/2005

Regulation - 648/2005 - EN - EUR-Lex (europa.eu)

9. Union Customs Code (UCC) Article 179

10. UCC Delegated Act (DA) Article 149

11. UCC Implementing Act (IA) Articles 229-232

12. UCC Transitional Delegated Act (TDA) Articles 18-20

13. Taxation and Customs Union – Online Services

Taxation and Customs Union - European Commission (europa.eu)

14. The Integrated Tariff (TARIC)

TARIC Consultation (europa.eu)

15. Enterprise Europe Network

Enterprise Europe Network | Enterprise Europe Network (europa.eu)

16. International Chamber of Commerce

Chamber International, export and import support for business (chamber-international.com)

17. Commission Implementing Regulation (EU) 2019/1793 of 22 October 2019 on the temporary increase of official controls and emergency measures governing the entry into the Union of certain goods from certain third countries implementing Regulations (EU) 2017/625 and (EC) No 178/2002 of the European Parliament and of the Council and repealing Commission Regulations (EC) No 669/2009, (EU) No 884/2014, (EU) 2015/175, (EU) 2017/186 and (EU) 2018/1660

Implementing regulation - 2019/1793 - EN - EUR-Lex (europa.eu)

Was this article helpful?