Tax Policy on Alcohol

- 3 Mins to read

- DarkLight

Tax Policy on Alcohol

- 3 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Malaysia

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 09 July 2024 | 12 July 2024 | N/A (new report) |

| V1 | 08 May 2025 | 03 June 2025 | All content has been reviewed and is still accurate. No updates were needed. |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol

1.1 Import Duty (Customs Duty)

Import Duty are defined in in Customs Duties Order 2022 [2], as below:

- Definition: A tax levied on the value of imported goods entering Malaysia.

- Rate: The rate is typically a percentage of the Cost, Insurance, and Freight (CIF) value of the goods. The CIF value includes the product's original price, insurance cost during transport, and freight charges.

- HS Code Dependence: The specific import duty rate depends on the product category and its Harmonized System (HS) Code. This internationally standardized system classifies traded goods. The HS Code for a product can be found through online resources or by contacting the manufacturer/supplier.

- Rate Determination: The Royal Malaysian Customs Department (RMCD) website provides a searchable database where you can find HS Codes and their corresponding import duty rates: https://www.customs.gov.my/en

1.2 Excise Duty

Excise Duty are defined in Excise Duties Order 2022 [3], as below:

- Definition: An indirect tax imposed on specific goods manufactured or imported for domestic consumption in Malaysia. It serves as a regulatory tool to influence consumer behavior and generate revenue.

- Applicable Goods: Excise duty applies to a limited range of goods, including [1]:

- Alcoholic beverages (beer, wine, spirits, etc.)

- Premix preparations

- Rate Structure: Excise duty rates vary significantly depending on the product category. For example, it is a percentage of the value of alcoholic beverages. The specific rates are published by the RMCD.

1.3 Sales Tax (SST)

- Sales tax administered in Malaysia is a single-stage tax imposed on the finished goods manufactured in Malaysia and goods imported into Malaysia.

- Sales tax on imported goods is charged when the goods are declared, duty paid, and released from customs control.

- 10% rate applied to the total value (CIF value + import duty + excise duty) for imported alcoholic beverages.

- Information on taxable goods and the current SST rate can be found on the MySST here [https://mysst.customs.gov.my/FAQSalesTax]

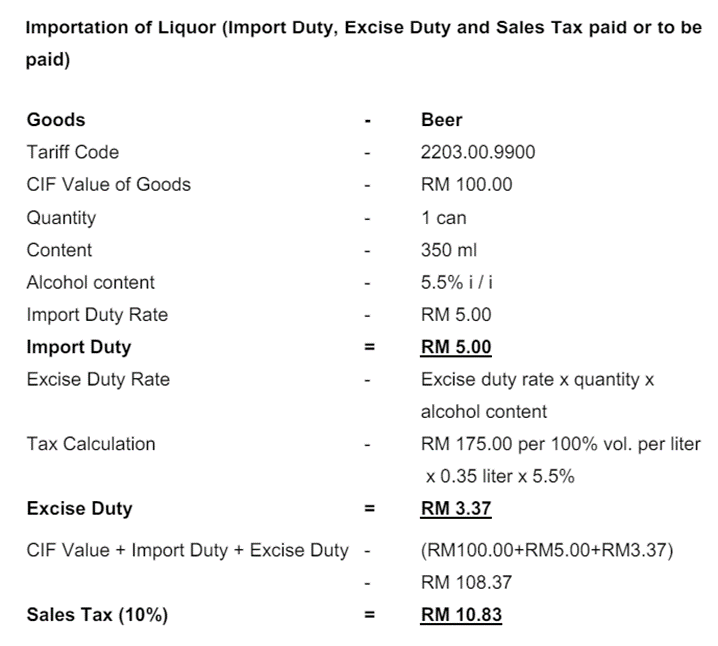

- The details calculation of Sales Tax for the Importation of liquor mentioned below can be referred to in the Guide on Manufacturing and Import/Export [4]:

2. Specific Requirements per Product

2.1 Beer, 4-7% alcohol

HS Code 2203.00; Beer made from malt

- Stout or porter:

- 2203.00.11 00 - Of an alcoholic strength by volume not exceeding 5.8% vol.

- 2203.00.19 00 - Other.

- Other, including ale :

- 2203.00.91 00 - Of an alcoholic strength by volume not exceeding 5.8 % vol.

- 2203.00.99 00 - Other.

Import Duty = RM 5/ litre

Excise Duty = RM175.00 x Volume (litre) x (alcohol %)

Sales Tax = 10% from CIF value + Import duty + Excise Duty

Please refer to the example of the calculation in Section 1.3 above.

2.2 Whisky, around 45% alcohol

HS Code 2208.30; Whiskies

- 2208.30.10 00 - In containers holding more than 5 l.

- 2208.30.90 00 - Other.

Import Duty = RM 58/ litre

Excise Duty = RM175.00 x Volume (litre) x (alcohol %)

Sales Tax = 10% from CIF value + Import duty + Excise Duty

Please refer to the example of the calculation in Section 1.3 above.

Conclusion

- Malaysia imposes three main taxes on imported alcoholic beverages, including beer and whisky: import duty, sales tax, and excise duty.

3. References

1. Malaysia Excise Custom official website

https://myexcise.customs.gov.my/myexcise/mengenai-eksais/

2. Customs Duties Order 2022

4. Guide on Manufacturing and Import/Export

PDF attached below

Was this article helpful?