Tax Policy on Alcohol

- 12 Mins to read

- DarkLight

Tax Policy on Alcohol

- 12 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Mongolia

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 12 Feb 2025 | 29 Mar 2025 | N/A (new report) |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol Goods

1.1 Tax framework for alcoholic beverages in Mongolia

• In Mongolia, the regulation and taxation of alcoholic goods are governed by a combination of laws and regulations designed to control the production, circulation, and taxation of alcohol while combating alcoholism. The primary legal frameworks include the Law on Control of the Circulation of Alcoholic Beverages and Combating Alcoholism [1], the Excise Tax Law [2], and specific orders governing the issuance of excise tax stamps [3].

• According to Article 37.2 of the Law on Control of the Circulation of Alcoholic Beverages and Combating Alcoholism, alcoholic beverages must bear an excise tax stamp when sold or served within Mongolia (except for export and customs-guaranteed zones). The sale or service of alcoholic beverages without such a stamp is prohibited [1].

• The Excise Tax Law applies to various goods, including alcoholic beverages, and establishes the tax rates and collection procedures for both domestically produced and imported products. The law defines different excise tax rates based on the type of alcoholic beverage—spirits, wine, or beer—and its alcohol content, with higher taxes imposed on stronger alcoholic beverages. It mandates that all alcoholic beverages sold in Mongolia must bear an excise tax stamp to ensure compliance with tax regulations, while also serving as a means of verifying the authenticity of the products. Additionally, the law imposes penalties for selling alcohol without an excise tax stamp, forging stamps, or failing to comply with tax registration procedures [2].

• The Order of the Minister of Finance, Issue A/12 establishes the model and issuance procedure for excise tax stamps in Mongolia, in accordance with Article 4, Section 4.3 of the Law on Excise Tax Stamps. The order approves the "Special Tax Mark Model" (Appendix 1) and the "Procedure for Issuing Special Tax Marks" (Appendix 2) [3].

1.2 Imposition of Excise Tax and Payment to the State Budget

• Imported Goods: The customs authority imposes excise tax on imported goods as they cross the Mongolian border.

• Excise tax on alcohol sold by alcohol producers must be paid to the state budget within 2 working days.

• When alcohol produced for food purposes is sold within Mongolia, buyers must receive a receipt with a unified serial number, as approved by the central state administrative body responsible for taxation.

• Excise Tax Deduction: For alcohol and wine produced and sold in Mongolia, the excise tax paid on the alcohol used in production may be deducted [2].

1.3 Excise tax exemption

The following goods are exempt from execution [2]:

- Exported Goods: Alcoholic beverages and other goods produced in Mongolia for export.

- Homemade Milk Alcohol: Alcohol distilled from milk and dairy products for personal use, produced using simple home-based methods.

- Duty-Free Alcohol: Alcohol imported in quantities allowed by customs for the personal use of passengers.

1.4. Format of Excise tax stamps for alcoholic beverages

• Excise tax stamps serve as proof that the company has fulfilled its tax obligations and provide the tax authorities with a clear record of the amount of alcoholic beverages that have been issued. This enables the authorities to monitor and track alcohol distribution effectively. The excise tax stamps also help prevent the circulation of counterfeit alcoholic beverages, which could pose health risks and result in lost revenue. [1, 2, 3].

• The excise tax stamp for alcoholic beverages, produced or imported into Mongolia, is rectangular, measuring 48mm by 16mm. However, for products under the duty-free shop regime, the stamp is either circular (30mm diameter) or oval (40mm by 30mm).

• Each stamp contains a unique 10-digit number and a high-security electronic data code (QR code) (10mm x 10mm) for tracking product details. Based on production and customs procedures, the stamp displays specific information, including a 3-letter code for the entity responsible for affixing it. Products in the free zone have a stamp marked "ЧБ" (Free Zone), while those in the duty-free regime display "ТБД" (Duty-Free Shop) [3].

• The background color of the stamp may vary depending on the production and customs procedures. Additionally, the stamp features a specialized metal insert that changes color under light and includes a hologram with four or more colors to further enhance security [3].

• The excise tax stamp must contain a unique, encrypted electronic data code. This code can only be decoded using devices approved by the tax authority or through the electronic payment receipt system. Consumers can use this code to access the relevant information via the system.

• Stamp paper must meet high-security standards, featuring a unique design, multi-colored threads (visible and ultraviolet), micro-cutting, and UV resistance. The ink used must comply with international security standards, enabling verification with specialized and regular devices. The adhesive must ensure secure attachment to various surfaces and prevent reuse or removal without damage.

• The excise tax stamp must be securely affixed to the packaging of alcoholic beverages in a manner that prevents tampering. The stamp is typically placed on the bottle cap or neck to make it visible and difficult to remove without causing damage [3].

Types of tax stamps [3]:

- For Locally Produced Products:

- Excise tax mark for Mongolian-made spirits (labeled as “АРХИ”).

- Excise tax mark for Mongolian-made wine (labeled as “ДАРС”).

- Excise tax mark for Mongolian-made tobacco (labeled as “ТАМХИ”).

- For Imported Products:

- Mark for imported spirits (“ИМПОРТЫН АРХИ”).

- Mark for imported wine (“ИМПОРТЫН ДАРС”).

- Mark for imported tobacco (“ИМПОРТЫН ТАМХИ”).

- For Free Zones and Duty-Free Shops:

- Mark for alcohol in free zones (“ЧӨЛӨӨТ БҮС АРХИ” or “ЧӨЛӨӨТ БҮС ДАРС”).

- Mark for alcohol in duty-free shops (“MONGOLIAN DUTY FREE”).

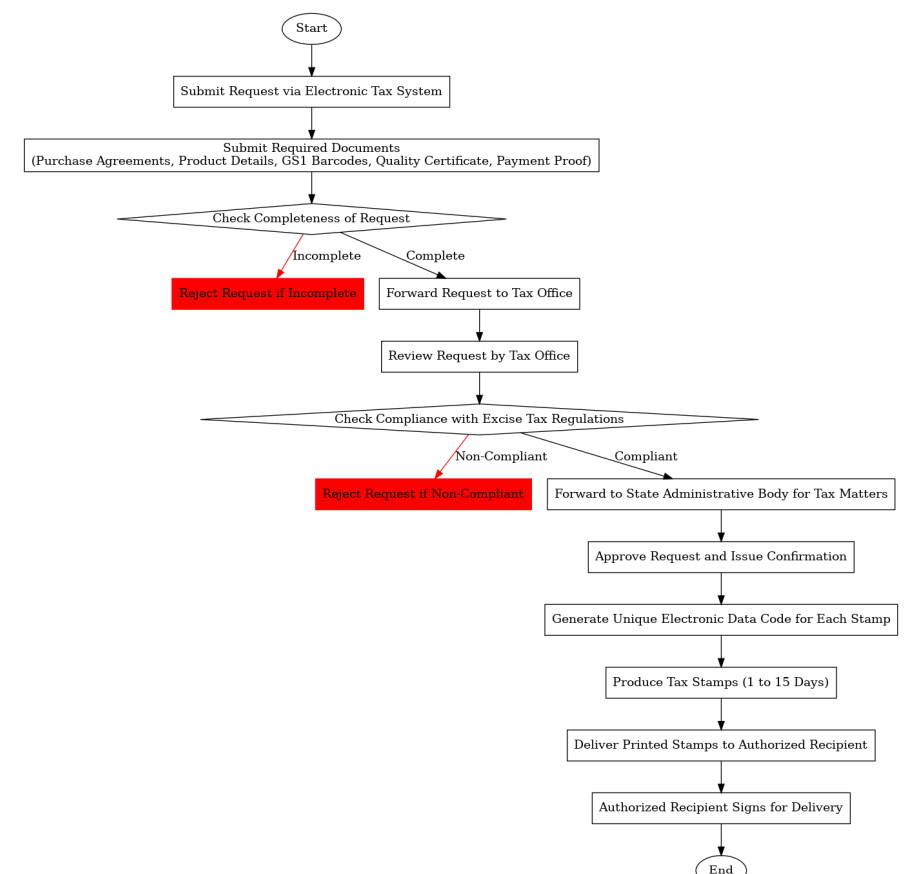

Procedure for Issuing Special Excise Tax Stamps [3]

Excise tax stamps are categorized for domestically produced alcohol, imported alcohol, tobacco, and duty-free goods. Manufacturers, importers, and duty-free shop operators are responsible for securely affixing the stamps in a tamper-proof manner. The procedure for Issuing Special Excise Tax Stamps includes the following main steps:

1. Request and Approval:

Entities must submit a request to the tax authorities with the required documentation (product details, contracts, proof of payment). The required documentation for requesting excise tax stamps includes:

- Official Request: Signed request with details on stamps, products, barcodes, and the authorized representative.

- Purchase Agreement: Copy of the agreement confirming product type and quantity, with a notarized translation if in a foreign language.

- Quality and Compliance Certificates: Proof of compliance with international standards and safety regulations.

- Proof of Payment: Confirmation of payment for the stamps.

2. Printing

Upon approval, the tax authorities generate a unique code for each stamp, which is printed according to international security standards. Printing time varies by order size, from 5 to 15 working days.

3. Delivery

The tax authorities will deliver the stamps to authorized representatives, with the delivery process documented to ensure accountability. The stamps must be registered in the electronic tax system and checked for compliance by customs authorities.

Figure 1. Flowchart illustrating the process for requesting, producing, and delivering Special Excise Tax Stamps

Figure 1. Flowchart illustrating the process for requesting, producing, and delivering Special Excise Tax Stamps

1.5. Excise tax rate for alcoholic beverages

The excise tax for all types of alcoholic beverages is calculated based on the volume (expressed in liter units) of the product. The total quantity of alcoholic beverages sold by producers in Mongolia serves as the tax base. If alcoholic beverages are transferred, donated, or used for personal purposes by individuals or companies, they are considered "sold" and subject to excise tax.

The excise tax rate is determined by the type, strength (alcohol content), and purpose of the alcoholic beverage. The rates are applied per liter and are periodically adjusted. Below are the applicable rates as of 2020 and beyond:

Table 1. The excise tax rate for alcoholic beverages prescribed by Article 6.1 The Law on Excise Tax [2]

| No | Title and type of goods subject to excise | Physical | Excise tax rate (MNT) (2020 and after thereof) | |

| 1 | Spirits for food use | Sold to a liquor factory | 1 liter | 1740 |

| Sold to pharmaceutical industry, human and veterinary use | 1 liter | 1450 | ||

| Sold elsewhere | 1 liter | 17400 | ||

| 2 | All types of brandy, whiskey, rum, and gin | Up to 25% | 1 liter | 8700 |

| 25-40 % | 1 liter | 17400 | ||

| 40% and more | 1 liter | 20880 | ||

| 3 | Domestically produced, industrially processed vodka | 1 liter | 350 | |

| 4 | All types of wines | Up to 35 % | 1 liter | 870 |

| 35 % and more | 1 liter | 7830 | ||

| 5 | All types of beer | 1 liter | 350 | |

The excise tax shall be imposed on physical units of all types of white alcohol, liqueurs, cordials, and other spirits drinks and all types of brandy, whiskey, rum, and gin at the following rates:

Table 2. The excise tax rate for white alcohol, liqueurs, cordials, cognac, whiskey, rum, gin, and other alcoholic beverages prescribed by Article 6.1 The Law on Excise Tax [2]

Title and type of goods subject to excise tax | Physical | Excise tax rate (MNT) | |||

| From 1 Jan 2025 to 1 Jan 2027 | From 1 Jan 2027 to 1 Jan 2029 | From 1 Jan 2029 and after thereof | |||

| All types of white alcohol, liqueurs, cordials, and other alcoholic beverages | Up to 25 % (includes Ready-to-drink beverages (mainly Chuhai), 3- 9% Alcohol | 1 liter | 3900 | 4100 | 4300 |

| 25-26 % | 1 liter | 7700 | 8100 | 8500 | |

| 26-28 % | 1 liter | 7700 | 8100 | 8500 | |

| 28-30 % | 1 liter | 7700 | 8100 | 8500 | |

| 30-32 % | 1 liter | 7700 | 8100 | 10440 | |

| 32-34 % | 1 liter | 7700 | 10440 | 13050 | |

| 34-36 % | 1 liter | 10440 | 11500 | 12600 | |

| 36-38 % | 1 liter | 11500 | 12600 | 13800 | |

| 38-40 % | 1 liter | 11500 | 12600 | 13800 | |

| 40% and more | 1 liter | 34450 | 37900 | 41690 | |

| All types of brandy, whiskey, rum, and gin | Up to 25 % | 1 liter | 9600 | 10100 | 10600 |

| 25-26 % | 1 liter | 19200 | 20200 | 21200 | |

| 26-28 % | 1 liter | 19200 | 20200 | 21200 | |

| 28-30 % | 1 liter | 19200 | 20200 | 21200 | |

| 30-32 % | 1 liter | 19200 | 20200 | 26100 | |

| 32-34 % | 1 liter | 19200 | 26100 | 28700 | |

| 34-36 % | 1 liter | 26100 | 28700 | 31600 | |

| 36-38 % | 1 liter | 28700 | 31600 | 34800 | |

| 38-40 % | 1 liter | 28700 | 31600 | 34800 | |

| 40% and more | 1 liter | 44000 | 50600 | 58200 | |

This tariff was added to the law as of July 6, 2022, and came into force on 1 Jan. 2023.

2. Specific Requirements on Tax Policy per Product

2.1 Capital City Tax applies to all kinds of alcoholic beverages

• In the capital city Ulaanbaatar, retailers of alcoholic beverages are subject to the Capital City Tax, as established under the Law on Capital City Tax (2015). This tax applies to alcoholic beverages sold in bars, restaurants, hotels, and other establishments such as holiday resorts, car washrooms, and taxi services within the capital and it is applied in addition to the excise tax [7].

• The tax rate is set at 2% of the value of goods sold, as determined by the Resolution of the Conference of Citizens' Representatives of the Capital, specifically Resolution No. 124, dated December 5, 2023 [8].

2.2 Beer

According to Article 6.1 of the Law on Excise Tax, the tax rate for all types of beer is 350 MNT per 1 liter [2].

2.3 Ready-to-drink beverages (mainly Chuhai*)

Table 3. The excise tax rate for other alcoholic beverages up to 25 percent prescribed by Article 6.1 The Law on Excise Tax [2]

| Title and type of goods subject to excise tax | Physical | Excise tax rate (MNT) | |||

| From Jan.1, 2023 to Jan.1, 2025 | From Jan.1, 2025 to Jan.1, 2027 | From Jan.1, 2027 to Jan.1, 2029 | From Jan.1, 2029 and after thereof | ||

| Other alcoholic beverages, also include Ready-to-drink beverages (mainly Chuhai*), 3-9% Alcohol | 1 liter | 3700 | 3900 | 4100 | 4300 |

2.4 Whisky

Table 4. The excise tax rate for whisky prescribed by Article 6.1 The Law on Excise Tax [2]

| Title and type of goods subject to excise tax | Physical | Excise tax rate (MNT) | ||||

| From Jan.1, 2023 to Jan.1, 2025 | From Jan.1, 2025 to Jan.1, 2027 | From Jan.1, 2027 to Jan.1, 2029 | From Jan.1, 2029 and after thereof | |||

| Whiskey | Up to 25 % | 1 liter | 9100 | 9600 | 10100 | 10600 |

| 25-26 % | 1 liter | 18300 | 19200 | 20200 | 21200 | |

| 26-28 % | 1 liter | 18300 | 19200 | 20200 | 21200 | |

| 28-30 % | 1 liter | 18300 | 19200 | 20200 | 21200 | |

| 30-32 % | 1 liter | 18300 | 19200 | 20200 | 26100 | |

| 32-34 % | 1 liter | 18300 | 19200 | 26100 | 28700 | |

| 34-36 % | 1 liter | 18300 | 26100 | 28700 | 31600 | |

| 36-38 % | 1 liter | 26100 | 28700 | 31600 | 34800 | |

| 38-40 % | 1 liter | 26100 | 28700 | 31600 | 34800 | |

| 40% and more | 1 liter | 38280 | 44000 | 50600 | 58200 | |

3. Taxes other than excise tax

In addition to the excise tax, alcoholic beverages in Mongolia are subject to the following taxes and regulatory requirements, as outlined in relevant laws and regulations:

3.1 Customs Duties for imported alcoholic beverages

• The customs duty on imported alcoholic beverages in Mongolia is governed by the Customs Law of Mongolia and the Resolution of the General Assembly of Mongolia on Approval of the Rate and Amount of Customs Duties on Imported Goods [4].

• According to Article 9.1.1 of the Customs Law, the taxable value for imported goods, including alcoholic beverages, is calculated by adding the customs value, customs duties, and excise tax [4].

• The rates and amounts of customs duties on imported goods are determined by the Resolution of the General Assembly of Mongolia on Approval of the Rate and Amount of Customs Duties on Imported Goods. For imported alcoholic beverages, the applicable rates and amounts are specified in Group 22 of the Annex to this resolution. The duty rates vary depending on the type of alcoholic beverage being imported [5].

3.2 Value-Added Tax (VAT)

The Value-Added Tax (VAT) on imported alcoholic beverages in Mongolia is regulated by the Law on Value-Added Tax of Mongolia. Article 7.1.2 of this law stipulates that VAT is imposed on all goods, works, and services imported into Mongolia from foreign countries. Article 11.1 establishes the VAT rate at 10%, which applies to the sales value of imported goods [6].

VAT Calculation for Imported Alcoholic Beverages

When alcoholic beverages are imported into Mongolia, VAT is calculated on the following basis:

VAT Taxable Value = Customs Value + Customs Duty + Excise Tax

The 10% VAT is then applied to this total value [6].

Conclusion

- In Mongolia, the taxation and regulation of alcoholic beverages are governed by a combination of laws and regulations designed to manage production, importation, and sales.

- The excise tax, which is based on the type and strength of the alcoholic beverage, is a key component of this regulatory framework.

- Excise tax stamps must be affixed to all alcoholic beverages sold within Mongolia, except for those intended for export or within customs-guaranteed zones, ensuring transparency and compliance with tax laws.

- Imported alcoholic beverages are subject to customs duties, excise tax, and Value-Added Tax (VAT).

- The Capital City Tax applies to alcoholic beverages sold within the capital city Ulaanbaatar, with a tax rate of 2% on the value of goods sold.

4. References

1. Law on control of the circulation of alcoholic beverages and combating alcoholism

https://legalinfo.mn/mn/detail?lawId=16530861302491

2. Law Of Mongolia on Excise Tax

https://legalinfo.mn/mn/edtl/16532054988521

3. Order of the Minister of Finance, Issue A/12, On approval of models and procedures of "Excise Tax Stamp Model” and the " Excise Tax Stamp Issuance Procedure"

https://legalinfo.mn/mn/detail?lawId=16758255986151

4. Law on Customs

https://legalinfo.mn/mn/detail?lawId=209

5. Resolution of the general assembly of mongolia on approval of the rate and amount of customs duties on imported goods

https://legalinfo.mn/mn/detail?lawId=6093

6. Law on Value-Added Tax

https://legalinfo.mn/mn/detail/11227

7. Law on Capital City Tax

https://legalinfo.mn/mn/detail?lawId=11193

8. Resolution of the conference of citizens' representatives of the capital on revised capital city official tax rate, December 5, 2023

https://legalinfo.mn/mn/detail?lawId=16960673720591

Was this article helpful?