Tax Policy on Alcohol

- 12 Mins to read

- DarkLight

Tax Policy on Alcohol

- 12 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Thailand

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 19 Feb 2025 | 4 Mar 2025 | N/A (new report) |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol Goods

In Thailand, the tax policy for alcoholic beverages is governed by various laws, primarily the Excise Tax Act and other related regulations. These laws outline the specific taxation framework that applies to the production, importation, and distribution of alcoholic beverages in Thailand. Below are the general requirements and key points regarding the tax policy on alcoholic beverages in Thailand:

- Import Tax

- Excise Tax

- Value Added Tax (VAT)

1.1 Import Tax

- Imported alcoholic beverages are subject to import tax. The import tax rate is determined by the Customs Department and applies to alcoholic beverages entering Thailand from foreign markets. Import duties are calculated based on the C.I.F. (Cost, Insurance, and Freight) value of the goods, which includes the product's cost, the shipping fees, and insurance costs.

- Importers must submit required documentation to Customs, including invoices, import declarations, and proof of payment of both excise and import taxes. The Customs Department collects the import tax when the goods enter the country. Import tax is typically assessed alongside excise tax at the point of importation.

- Import duty rates are determined based on the Harmonized System (HS) codes assigned to each group of goods. For alcoholic beverages, the applicable tax rates are outlined in Chapter 22: “Beverages, Spirits, and Vinegar” of Part 2: “Import Duty Tariff” of the Account to the Royal Decree on Customs Tariffs (No. 7) B.E. 2564 [1, 2].

Note that for Chapter 22 “Beverages, Spirits, and Vinegar”, the” alcoholic strength by volume” is determined at a temperature of 20°C.

1.2 Excise Tax

- Excise tax is an indirect tax levied on certain goods, whether manufactured in Thailand or imported. Industrialists, importers, service providers, or any other parties liable under the Excise Act B.E. 2560 are required to pay excise tax based on the applicable and valorem duty, specific duty, or both, as specified in the attached schedule. The rate applied will be the one in effect when the excise liability arises [3].

- For goods, the excise tax on an ad valorem basis is calculated using the suggested retail price (excluding VAT), which reflects production costs, management expenses, and standard profit margins. The price should not be lower than the amount paid by the last consumer in a typical market, in accordance with the Ministerial Regulations. If the suggested retail price is impractical, inconsistent with market dynamics, or undetermined, the Director-General of the Excise Department may establish the price using the sales or import price, in accordance with the Ministerial Regulations [3].

- Excise liability on imported goods begins when import duties are imposed under customs law. If goods are stored in a bonded warehouse, free zone, or free-trade zone, the excise tax liability arises when the goods are removed from these locations. Consumption of such goods within these zones by the importer or any other party will also trigger the excise tax liability, as if the goods were taken out of the bonded warehouse or free zone [3].

- For imported liquor*, excise tax is applied either at a specific rate (based on quantity or volume ) or an ad valorem rate (a percentage of the product's value) [3].

*"Liquor" refers to any material or mixture containing alcohol that can be consumed either on its own or when mixed with other liquids, excluding beverages with less than 0.5% alcohol by volume. "Fermented liquor" means non-distilled liquor, including fermented liquor mixed with distilled liquor, containing less than 15% alcohol by volume. "Distilled liquor" refers to distilled spirits, including distilled spirits mixed with fermented liquor, containing more than 15% alcohol by volume.

The tax rates for alcoholic beverages and other excise-taxable goods are specified in the Ministerial Regulations on Excise Tax Rates 2017 [4], as amended by Ministerial Regulations No. 02 and Ministerial Regulations No. 32 [5, 6]. Companies can access the updated tax rates in the consolidated notifications issued by the Excise Department via the link https://lawelcs.excise.go.th/lawdetail?id=6656 [7].

Additional Taxes and Funds Applicable to Liquor

In addition to the excise tax, liquor products are subject to additional levies and contributions to various funds designated for specific purposes. These include:

- Municipality Tax: 10% of the excise tax, collected for the Ministry of Interior [8].

- Thai Health Promotion Foundation (ThaiHealth): 2% of the excise tax [9, 10].

- Public Broadcasting Service of Thailand Fund (Thai PBS): 1.5% of the excise tax [11].

- National Sports Development Fund (SAT): 2% of the excise tax [12].

- Excise Tax Fund (Elderly Fund): 2% of the excise tax [13].

These contributions ensure that the tax burden on liquor also supports public health, broadcasting, sports development, and local government initiatives.

Calculation of Liquor Tax [14]

Liquor products in Thailand are subject to two forms of taxation: ad valorem (based on value) and volumetric (based on quantity). The tax payable combines these two methods, and the suggested retail price (excluding VAT) is used as the basis for calculating the excise tax instead of production costs (excluding liquor stamps). Below is the detailed process for calculating liquor taxes:

1) Calculation of the Excise Tax Based on Value

Excise Tax (Value)=Retail Price (excluding VAT) × Ad Valorem Tax Rate

2) Calculation of the Excise Tax Based on Volume

Excise Tax (Volume)=Alcohol Strength (degrees)×Container Size (liters)×Volumetric Tax Rate

3) Determination of the Total Excise Tax

Total Excise Tax=Excise Tax (Value)+Excise Tax (Volume)

4) Calculation of the Contributions to Specific Funds

Contributions are calculated as a percentage of the total excise tax:

- Health Promotion Fund (ThaiHealth): 2%

- ThaiHealth Fund=Total Excise Tax×2%

- Sports Development Fund (SAT): 2% SAT

- Fund=Total Excise Tax×0.02

- Public Broadcasting Service of Thailand (Thai PBS): 1.5%

- Thai PBS Fund=Total Excise Tax×0.015

- Elderly Fund: 2%

- Elderly Fund=Total Excise Tax×0.02

5) Calculation of the Local Government Tax Surcharge

- Municipality Tax: 10%

- Local Government Surcharge=Total Excise Tax×0.1

6) Calculation of the Total Net Excise Tax Payable

The total amount payable is the sum of the total excise tax and all contributions:

1.3 Value Added Tax (VAT) [15, 16]

- VAT is an indirect tax applied to the value added to goods and services at each stage of production and distribution. It affects retailers, manufacturers, wholesalers, producers, importers, and service providers. Introduced in Thailand in 1992 to replace the Business Tax (BT), VAT is levied on the value added throughout the production and distribution process.

- The tax base for VAT is the total value received or receivable from the supply of goods or services. "Value" includes money, property, consideration, service fees, or any other benefits that can be quantified in monetary terms. The tax base also includes any excise tax related to the supply, but excludes VAT itself, as well as any discounts or allowances, unless explicitly specified in the tax invoice.

- Any individual or entity regularly supplying goods or providing services in Thailand with an annual turnover exceeding 1.8 million baht is subject to VAT. Services are considered provided in Thailand if performed within the country, regardless of where they are utilized, or if performed abroad but used within Thailand.

- Under VAT, taxable goods encompass all types of property, whether tangible or intangible, and include goods for sale, personal use, or any other purposes. This also applies to articles imported into Thailand. Services refer to any activities conducted for the benefit of an individual or entity that are not categorized as goods.

- Tax Rates: The standard VAT rate is 7%.

- Imported Goods: Importers are subject to VAT in Thailand, with VAT collected by the Customs Department at the time of import. VAT filings and payments must be submitted to the Customs Department during the import process.

- The tax base for imported goods is calculated as follows:

- Tax Base = C.I.F. price + Import duty + Excise tax (if any) + Other taxes and fees (if any)

2. Specific Requirements on Tax Policy per Product

2.1 Beer

In Thailand, imported alcoholic beverages are subject to specific regulations concerning excise stamps, as outlined by the Excise Department under the Ministry of Finance. According to Section 64, paragraph two of the Excise Tax Act B.E. 2560 (2017), the use of excise stamps and tax payment marks to indicate that tax has been paid must follow the criteria, methods, and conditions specified in the Ministerial Regulations [3].

It mandates that all alcoholic beverages bear excise stamps as proof of tax payment. Importers are required to apply for excise stamps prior to bringing alcoholic beverages into Thailand. Excise stamps must be affixed to each bottle or container of alcoholic beverage [17].

Regulations on the Affixing of Tax Stamps on Alcoholic Beverage Products [17]

- For all types of liquor, except as stated in Section 2:

- Excise stamps must be adhesive-backed.

- Moisten the adhesive and firmly apply the stamp over the mouth of the liquor container, ensuring it cannot be removed without destruction.

- The excise stamp must be positioned so that it is immediately destroyed upon opening the container.

Specific cases:

- For bottled liquor, the excise stamp must be placed across the bottle cap or stopper, with its edges securely sealed along the neck of the bottle.

- If the excise stamp cannot fully cover the mouth of the liquor container, use a paper sheet three times larger than the lid to cover the opening.

- Secure the paper tightly with wire, sealing the knot with lac or lead, and affix the excise stamp over the sealed knot. Ensure the stamp fully adheres along the mouth of the container and will be destroyed upon opening.

- For liquor in aluminum foil bags or other containers with pour stoppers, packaged within a box (paper or other material):

- The box must have a printed name or trademark and perforations that can be torn to access the stopper.

- Apply adhesive fully to the back of the excise stamp, then firmly affix it along the perforated edge of the box so it cannot be peeled off.

- The excise stamp must be destroyed immediately when the box is torn open to access the liquor container.

Types and characteristics of excise stamps [18]

Types of Excise Stamps:

- Excise Stamp for domestically produced alcohol

- Excise Stamp for imported alcohol

- Excise Stamp for alcohol produced or imported into the Kingdom, displayed and sold in bonded warehouses located at international airports for travelers entering the Kingdom.

General Features of the Excise Stamp for Imported Alcohol:

- Material: Made from white or off-white paper with a clear-glass back sheet.

- Dimensions: Rectangular, measuring 1.5 x 12.5 cm.

- Anti-Counterfeiting Measures:

- Printed with red and orange ink.

- The text "EXCISE DEPARTMENT" appears in red across the entire stamp.

- The left and right sides contain the phrase "Excise Department" in red.

- The center features the Excise Department symbol in raised silver ink.

- Raised silver ink is used for Thai text displayed on either side of the symbol.

- A QR code and anti-counterfeiting features visible under ultraviolet light.

- The volume and alcohol proof are printed in black ink.

Example:

Figure 1. Stamp format for all types of liquor imported into Thailand [8]

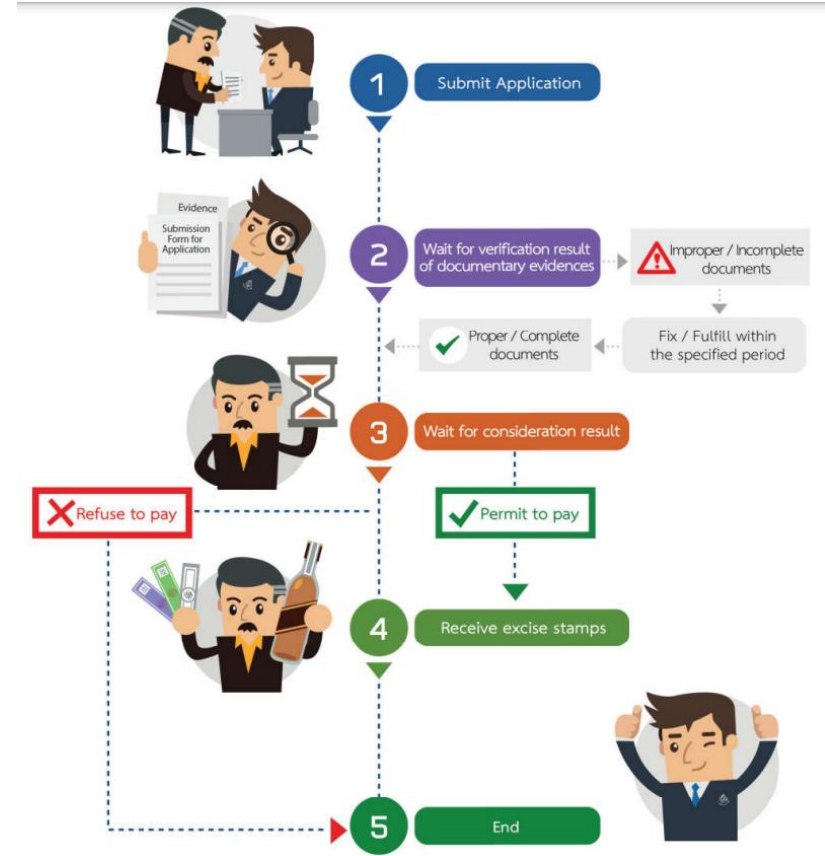

Application for Excise Stamps for Imported Liquor [17, 19, 20]

Applications for excise stamps can be submitted at the following locations:

- Area Excise Office

- Excise Office, Branch Area

Application form: Por Sor 06-12. To request the form, applicants may contact Excise Department (Central), Regional Excise Office, Area Excise Office, or Excise Department Branch Office or download from this link. Qualifications for Applicants must hold a Type 1 Liquor Sales License and must have paid excise tax for the liquor requiring excise stamps.

Characteristics of Liquor Requiring Excise Stamps:

- Liquor imported into the Kingdom for sale.

- The importer must hold a valid license to import liquor into the Kingdom.

Application Process

1. Submission:

Submit Form Por Sor 06-12 along with all required supporting documents to the local excise office where the product release procedure unit is located.

List of Supporting Documents for Application Submission:

- ID Card (For individual): 1 original copy

- Certificate from the Ministry of Commerce, issued within the last 6 months (for business entity): 1 copy

- Import Declaration: 1 original copy

- Tax Receipts (Total Tax Paid): 1 original copy

- License to Import Liquor into the Kingdom: 1 original copy

- Product List and Price List (Invoice): 1 original copy

- Identity documents authorizing another person, if applicable

- Power of attorney, affix stamp duty as required by law: 1 original copy

- Identity card of the person granting the power of attorney, signed, and certified true copy: 1 copy

- Identity card of the attorney, signed, and certified true copy: 1 copy

2. Examination:

The excise office will review the application and supporting documents. If the submission is correct and complete, the applicant will receive approval to obtain excise stamps for the imported liquor.

Total Processing Time: The total processing time will not exceed 2 hours from the date the supporting documents are received correctly and completely.

Fees: No fees required [19, 21]

Figure 2. Application Process for Excise Stamps for Imported Liquor [19]

2.2 Ready-to-drink beverages (mainly Chuhai*)

Same as “Beer” above.

2.3 Whisky

Same as “Beer” above.

3. Additional Information

None.

Conclusion

- Thailand's liquor taxation framework is a comprehensive and structured system encompassing multiple tax components, including customs duties, excise taxes, VAT, and additional levies earmarked for societal initiatives.

- Customs duties, governed by the Customs Tariff Act, apply specific rates to imported goods based on HS codes.

- Excise taxes, a central aspect of this framework, are imposed on both imported and domestically produced beverages.

- VAT, standardized at 7%, applies to the retail price of liquor.

- Liquor products are subject to supplementary taxes and contributions aimed at supporting various societal initiatives. These include the Municipality Tax, Public Broadcasting Service of Thailand Fund, the National Sports Development Fund, and the Excise Tax Fund for elderly care.

- The regulatory requirements, including precise excise stamp usage, ensure compliance and facilitate effective tax collection.

4. References

1. Customs Tariff Act (No. 7) B.E. 2564

https://www.customs.go.th/data_files/b36b588aed6b9d086e88c0d5fb9ae7a2.pdf

2. Text of AHTN 2017 with Corrigendum (English Tariffs for Reference)

https://www.customs.go.th/data_files/3a4ffe38a9a5a67e1e4724218016c369.pdf

3. EXCISE ACT B.E. 2560 (2017)

https://lawelcs.excise.go.th/img/Excise_Act_EN.pdf

4. Ministerial Regulations Excise Tax Rates 2017

https://www6.excise.go.th/portal/ExciseTax/law_1/AA_000027.pdf

5. Excise Tax Rate Regulations (No. 2) B.E. 2017

https://www6.excise.go.th/portal/ExciseTax/law_1/AA_000028.pdf

6. Ministerial Regulations on Tax Rates (No. 32) B.E. 2023

https://www6.excise.go.th/portal/ExciseTax/law_1/AA_000069.pdf

7. Excise Tax Rate List - Part 13 Liquor

https://lawelcs.excise.go.th/lawdetail?id=6656

8. Excise tax collection management - Liquor by Ms. Suphatrada Thong-on, Director of Tax Standards and Development Division 1

https://www.excise.go.th/cs/groups/public/documents/document/dwnt/ndg4/~edisp/uatucm488923.pdf

9. Ministry of Finance regulations Concerning the collection, remittance, exemption and refund of the Health Promotion Fund for alcohol and tobacco. 2001

10. Thailand Health Promotion Fund Resource Hub website

11. Excise Department Regulations on the Transfer of Money and Collection of Public Broadcasting Service of Thailand's Maintenance Fee for Alcohol and Tobacco B.E. 2559 (2016)

https://www.ratchakitcha.soc.go.th/DATA/PDF/2559/D/022/1.PDF

12. Ministry of Finance regulations Regarding the collection, remittance, exemption and refund of the National Sports Development Fund for alcoholic beverages and tobacco 2015

13. Regulation of the Ministry of Finance On the collection, remittance, exemption, reduction and refund of the Elderly Fund Maintenance Fund for alcoholic and tobacco products B.E. 2561 (2018)

https://www.dop.go.th/download/knowledge/th1714465173-2536_0.pdf

14. Liquor tax calculation

https://www.excise.go.th/cs/groups/public/documents/document/dwnt/ndi1/~edisp/uatucm425661.pdf

15. Value Added Tax (VAT)

https://www.rd.go.th/english/6043.html

16. Category 4 Value Added Tax

https://www.rd.go.th/2596.html

17. Excise Department Announcement Re: Regulations on the use, cancellation and closing of excise stamps for liquor products 2018

https://www.ratchakitcha.soc.go.th/DATA/PDF/2561/E/119_2/135.PDF

18. Ministerial Regulations Determining the types and characteristics of excise stamps and government tax payment marks B.E. 2563 (2020)

https://webdev.excise.go.th/act2560/files/legal/T_0001.PDF

19. Application for Receiving Excise Stamps for Liquor that is Imported into the Kingdom for Sale

https://edmanual.excise.go.th:50001/document/pdf/ED04-0004-M4

20. Requests for Licenses Obtaining permission to import liquor into the Kingdom

21. Ministry Regulations Prescribing Fees and Exemptions from License Fees under the Excise Tax Act B.E. 2560

https://lawelcsuat.excise.go.th/lawdetail?id=5749

Was this article helpful?