Tax Policy on Alcohol

- 3 Mins to read

- DarkLight

Tax Policy on Alcohol

- 3 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Indonesia

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 10 Feb 2025 | 12 Feb 2025 | N/A (new report) |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol Goods

In Indonesia, the Ministry of Finance (MoF) is the authority responsible for overseeing national policies and regulations related to taxes and duties on all trade goods. Specifically, in the case of alcoholic products, MoF focuses on determining the duty tariffs (local language: cukai) for alcoholic goods, including alcoholic beverages.

The Ministry of Finance (MoF) sets the tax and duty tariffs for alcoholic goods under Ministry of Finance Decree No. 160 of 2023 on Duty Tariffs for Ethyl Alcohol, Beverages Containing Ethyl Alcohol, and Concentrates Containing Ethyl Alcohol [1]. The key points of the regulation include the establishment of duty tariffs for:

- Ethyl Alcohol (or ethanol)

- Beverages containing ethyl alcohol (including alcoholic beverages)

- Concentrates containing ethyl alcohol

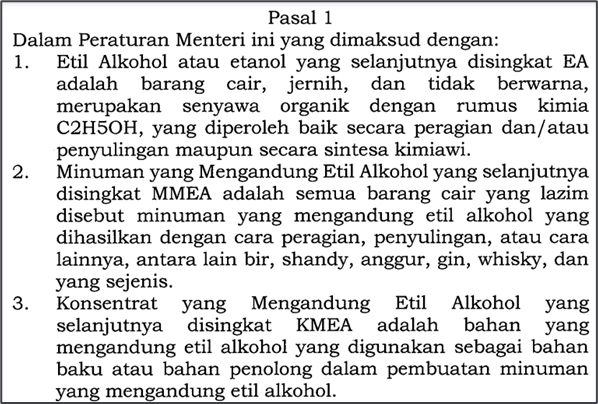

Figure 1. Excerpt of Ministry of Finance Decree No. 160 of 2023 [1]

The duty tariffs for alcoholic goods are outlined in Articles 2-4 and are clearly listed in the Annex of Ministry of Finance Decree No. 160 of 2023 [1]:

- Ethyl alcohol or ethanol

Class | Ethyl alcohol content | Duty tariff (per liter) | |

Domestic product | Import product | ||

No Class | At any content | IDR 20,000 (USD 1.25) | IDR 20,000 (USD 1.25) |

- Beverages Containing Ethyl Alcohol

Class | Ethyl alcohol content | Duty tariff (per liter) | |

Domestic product | Import product | ||

A | Up to 5% | IDR 16,500 (USD 1.05) | IDR 16,500 (USD 1.05) |

B | >5 – 20% | IDR 42,500 (USD 2.68) | IDR 53,000 (USD 3.35) |

C | >20 – 55% | IDR 101,000 (USD 6.38) | IDR 152,000 (USD 9.60) |

- Concentrates Containing Ethyl Alcohol

Class | Type of concentrate containing ethyl alcohol | Duty tariff | |

Domestic product | Import product | ||

No Class | Liquid form | IDR 228,000 (USD 14.40) per liter | IDR 228,000 (USD 14.40) per liter |

No Class | Solid form | IDR 1,000 (USD 0.06) per gram | IDR 1,000 (USD 0.06) per gram |

Notes

USD values are estimated based on the current exchange rate as of the date of this report.

2. Specific Requirements on Tax Policy per Product

2.1 Beer

Beer that contains 4-7% alcohol may be classified into Class A (ethanol content up to 5%) or Class B (ethanol content >5 – 20%). The duty tariff can refer to table number 2 (Beverages containing ethyl alcohol) in Section 1 above.

2.2 Ready-to-drink beverages (mainly Chuhai*)

Ready-to-drink alcoholic beverages (mainly Chuhai) may be classified into Class A (ethanol content up to 5%), Class B (ethanol content >5 – 20%), or Class C (ethanol content >20 – 55%). The duty tariff can refer to table number 2 (Beverages containing ethyl alcohol) in Section 1 above.

2.3 Whisky

Whisky that contains around 45% alcohol may be classified into Class C (ethanol content >20 – 55%). The duty tariff can refer to table number 2 (Beverages containing ethyl alcohol) in Section 1 above.

Conclusion

- In Indonesia, the Ministry of Finance (MoF) is the authority responsible for setting the tax and duty tariffs for alcoholic goods under Ministry of Finance Decree No. 160 of 2023 on Duty Tariffs for Ethyl Alcohol, Beverages Containing Ethyl Alcohol, and Concentrates Containing Ethyl Alcohol.

- The duty tariffs are applied for:

- Ethyl Alcohol (or ethanol)

- Beverages containing ethyl alcohol (including alcoholic beverages)

- Concentrates containing ethyl alcohol

- Beer, ready-to-drink alcoholic beverages (mainly Chuhai), whisky, and other alcoholic beverages fall under the category of beverages containing ethyl alcohol. The applicable duty tariffs are outlined in Table 2 of Section 1, with the specific rates varying depending on the class of the alcoholic beverages:

- Beer: Class A or B

- Ready-to-drink alcoholic beverages (mainly Chuhai): Class A, B, or C

- Whisky: Class C

3. References

1. The Ministry of Finance Decree No.160 Year 2023 on Duty Tariffs on Ethyl Alcohol, Beverages Containing Ethyl Alcohol, and Concentrates Containing Ethyl Alcohol

https://jdih.kemenkeu.go.id/download/fa52d458-cdd7-4554-aed2-7a649331bb40/2023pmkeuangan160.pdf

Was this article helpful?