Tax Policy on Alcohol

- 5 Mins to read

- DarkLight

Tax Policy on Alcohol

- 5 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

UK

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 20 June 2024 | 24 June 2024 | N/A (new report) |

| V1 | 21 May 2025 | 30 May 2025 | Full review of the report to reflect updates made in 2025, mainly: ending the alcohol duty stamp scheme, updating alcohol duty rates and alcohol duty system, and revising import requirements. |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements

1.1 Alcohol Duty

Alcohol Duty is the excise duty that is payable on all beer, cider, wine, or other fermented products (known as ‘made wine’) and spirits. It is defined by Article 47 of the Finance (No.2) Act 2023 [1].

Figure 1 – Legal Definition of Alcohol Duty

Figure 1 – Legal Definition of Alcohol Duty

Duty is levied according to the strength of the alcohol rather than the type of alcohol. This aims to encourage drinkers to cut back on their weekly units of alcohol by taxing alcohol based on strength (i.e. the higher the strength, the higher the duty and the higher the cost of the product).

The rates of duty apply to all alcoholic products produced in, or imported into, the UK. It is payable by the company that produces the drinks in the UK or imports the drinks into the UK.

Duty rates are set out within the Finance (No.2) Act 2023 [1], (Part 2) and Schedule 7, Table 1. The rates set in Spring 2023 were frozen until February 2025. Normally alcohol duties are increased in line with the Retail Price Index (RPI) inflation on 1 February annually, and this was re-introduced by the budget in the Autumn of 2024, with changes taking effect from 1 February 2025.

The UK government changed to this way of calculating duty in August 2023 and the House of Commons Library published an explanatory document explaining the changes [2].

When importing alcohol into the UK, such goods become liable for UK Excise Duty (alcohol duty) once the goods arrive in the UK. Excise duty is not payable at that point if one of the following applies on import:

- It is delivered into an excise warehouse approved for that purpose.

- It is delivered into a customs warehouse which has a separate excise warehouse approval for those premises.

- You are a registered brewer and you receive alcohol into your registered premises of a class that your registration entitles you to hold.

Since 1 February 2025, you can apply for an alcoholic products producer approval (APPA), to make sure your premises are improved to import and hold all alcoholic products in duty suspension. Payment of Alcohol Duty can be suspended in the following circumstances:

- You are importing alcoholic products directly into your approved premises, as you hold an APPA and are approved to receive alcoholic products produced elsewhere in duty suspension.

- The imported alcoholic product is delivered directly to an excise warehouse for the receipt of alcoholic products.

This is further explained in the UK government guidance ‘Import alcohol into the UK’ [3].

1.2 VAT

Value Added Tax (VAT) is also chargeable on the duty-inclusive price at the standard rate of 20% on alcohol products.

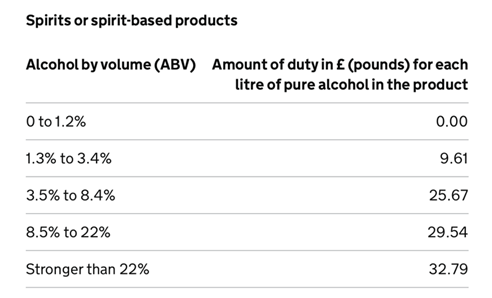

Figure 2. Excerpt of the updated alcohol duty rates published by HM Revenue and Customs [1.1]

2. Specific Requirements for Whisky

2.1 Alcohol Duty

As the alcohol duty is calculated based on alcoholic strength, there are no specific requirements for whisky.

Whisky, around 45% alcohol

To calculate the duty for a 1 litre whisky of 45% abv:

- 45% of 1 litre = 0.45 litres of pure alcohol

- 0.45 litres of pure alcohol x £32.79 (the duty rate) = £14.76 duty to pay

2.2 Third-Country Duty for Whisky Imported from Japan

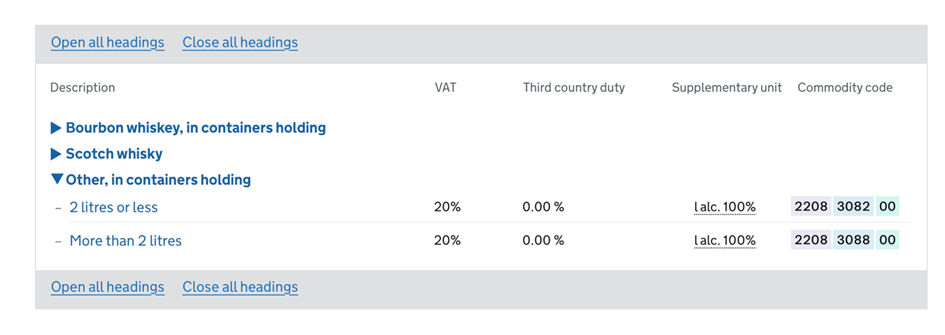

Whisky over 22% ABV in containers of 2 litres or less have commodity code 2208 3082 00 and above 2 litres have commodity code 2208 3088 00. They are not liable for third-country duty due to the trade agreement between Britain and Japan. However, they may have to provide a certificate or proof of preferential origin to claim this preferential duty rate. This would need the assistance of a customs consultant.

Figure 3. Source UK Trade Tariff website: Commodity code 2208 30 – Whiskies [4]

Figure 3. Source UK Trade Tariff website: Commodity code 2208 30 – Whiskies [4]

3. Other rules

From 1 May 2025, there is no need to register, obtain, or apply Alcohol Duty stamps to retail containers previously covered by the scheme. Registrations and authorizations under the scheme will automatically end, without any action needing to be taken. However, existing records for retail containers stamped before the scheme’s end must be kept for at least 3 years from the date that the record was made. [5]

Conclusion

- In the UK, alcohol is liable to both alcohol duty tax, which is a form of excise duty payable on alcoholic products, and value-added tax (VAT).

- Alcohol duty tax is based on the strength of the alcohol and is payable by the company that imports the drinks.

- For Alcohol over 22% ABV, the alcohol duty tax is £32.79 per liter of pure alcohol in the product.

- When they are sold in the UK, alcoholic drinks including imported whisky are liable for value-added tax (VAT) which is then payable by the final customer on the price including the alcohol duty, VAT is charged at 20% of the selling price.

4. References

1. Finance (No. 2) Act 2023

https://www.legislation.gov.uk/ukpga/2023/30

1.1 Updated Alcohol Duty Rates published by HM Revenue and Customs

https://www.gov.uk/guidance/alcohol-duty-rates

2. House of Commons – new alcohol duty system

https://researchbriefings.files.parliament.uk/documents/CBP-9765/CBP-9765.pdf

3. Guidance ‘Import alcoholic products into the UK', updated in 2025

https://www.gov.uk/guidance/import-alcohol-into-the-uk

4. UK Trade Tariff: Commodity Code 220830 – Whiskies

https://www.trade-tariff.service.gov.uk/subheadings/2208300000-80?day=2&month=5&year=2025

5. Ending the Alcohol Duty Stamp Scheme

https://www.gov.uk/government/publications/revenue-and-customs-brief-1-2025-ending-the-alcohol-duty-stamp-scheme/ending-the-alcohol-duty-stamp-scheme

Was this article helpful?