Tax Policy on Alcohol

- 8 Mins to read

- DarkLight

Tax Policy on Alcohol

- 8 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

China

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 26 Jan 2024 | 28 Feb2024 | N/A (new report) |

| V1 | 17 April 2025 | 21 May 2025 | Overall update (including the introduction of a new Tariff Law replacing the previous regulations) and insights for 2025. |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements for All Goods

1.1 Requirement

According to Article 2 of the “Customs Law” [1] and Articles 3, 13, and 20 of the "Administrative Measures for the Levy of Import and Export Duties" [2], the taxpayer of imported alcoholic beverages (typically the consignee of the imported goods) is required to declare customs duties to the customs within a prescribed period when importing goods. Customs duties covered:

- Taxation authority: General Administration of Customs (GACC)

- Tax item details: Tariffs are collected by the customs, while VAT (value-added tax) and Consumption Tax in the import process are collected by the customs on behalf of the taxation authority

1.2 Calculation Methods for Tariff, Consumption Tax, and VAT

According to the provisions of Chapter 2 of the "Administrative Measures for the Levy of Import and Export Duties" [2] after determining the classification of goods, dutiable value, and country of origin, the Customs will levy import-related taxes on imported goods based on the applicable tax types, tax items, tax rates, and calculation formulas stipulated by relevant laws and administrative regulations.

(1) Calculation formulas based on value:

- Tariff = Dutiable Value * Tariff Rate

- Consumption Tax= [(Dutiable Value + Tariff) / (1 - Consumption Tax Rate)] * Consumption Tax Rate

- VAT = (Dutiable Value + Tariff + Consumption Tax) * VAT rate

- Total taxes = Tariff+ Consumption Tax+ VAT

(2) Calculation formulas based on quantity:

- Tariff = Quantity of Goods * Unit Tariff Rate amount

- Consumption Tax = Quantity of Goods * Unit Consumption Tax Rate Amount

- VAT = (Dutiable Value + Tariff + Consumption Tax) * VAT rate

- Total taxes = Tariff+ Consumption Tax+ VAT

Dutiable Value is examined and determined by the customs, commonly known as Cost Insurance and Freight (CIF) price.

According to the "Provisional Regulations on Consumption Tax of the People's Republic of China" [3] and the "Tax Rate Table for Consumption Tax" in the appendix, Consumption Tax applies to several goods regardless imported or not, including alcoholic beverages.

1.3 Sequence of Application for Tariff Rates

According to Article 13 of the "Tariff law" [4] for imported goods subject to the most-favored-nation (MFN) tariff rate and having provisional tariff rates, the provisional tariff rates should be applied. For imported goods subject to conventional tariff rates or preferential tariff rates and having provisional tariff rates, the lower applicable tariff rate should be applied. Imported goods subject to general tariff rates do not apply provisional tariff rates.

The Tariff law [4] has entered into force as of December 1, 2024, replacing the previous Regulations of Import and Export Customs Duties.

Below are the definitions for different types of Tariff rates:

- MFN (Most-Favored-Nation Tariff) Rate: Countries or regions that have signed bilateral trade agreements with China containing provisions on mutual most-favored-nation treatment, including WTO members. [7]

- Conventional Tariff Rate: Countries or regions [8] that have signed regional trade agreements with China containing provisions on tariff preferences.

- Preferential Tariff Rate: Imported goods from countries or regions [8] that have signed special preferential tariff agreements with China.

- Provisional Tariff Rate: Temporarily adjusted tariff rates to be implemented.

- General tariff rate: Countries or regions not mentioned above.

2. Specific Requirements for Alcoholic Beverages (Examples)

2.1 Beer, 4-7% Alcohol

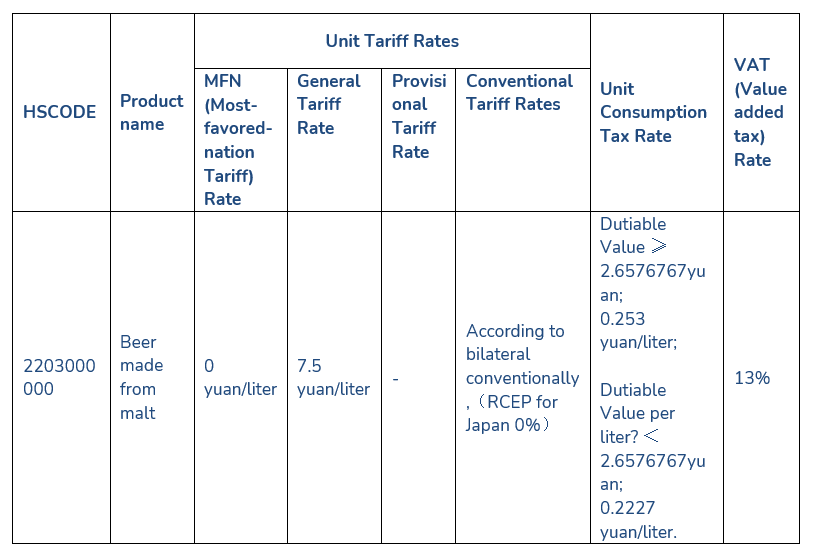

According to Chapter 22 of the "Explanatory Notes to the Customs Tariff of Import and Export" [5], the goods are highly likely to be classified under 2203000000.

Source: The above tax rates are sourced from the official website of the General Administration of Customs (GACC) [6] as of April 17, 2025.

Table 1. Different tax rates for Beer from the official website of the General Administration of Customs (GACC)[6]

For example: Assuming that the Country is Japan which is the most-favored nation, and a member of RCEP, the quantity of its imported beer is 1000 liters. The Dutiable Value (CIF) is 2700 yuan.

Tariff = Quantity of Goods * Unit Tariff Rate amount

= 1000 liters * 0 yuan/liter

= 0 yuan (Based on quantity: MFN rate is 0 yuan/liter)

Consumption Tax =Quantity of Goods * Unit Consumption Tax Rate Amount

= 1000 liters * 0.253 yuan/liter

= 253.00 yuan (Based on quantity: 2700/1000 = 2.7 yuan/liter, which is ≥2.6576767 yuan, so the rate of 0.253 yuan/liter applies).

VAT= (Dutiable Value + Tariff + Consumption Tax) * VAT rate

= (2700 + 0 + 253) * 13%

= 383.89 yuan.

Total taxes = Tariff + Consumption Tax+ VAT

= 0 + 253 + 383.89

= 636.89 yuan.

2.2 Ready-to-drink Beverages (mainly Chuhai), 3-9% Alcohol

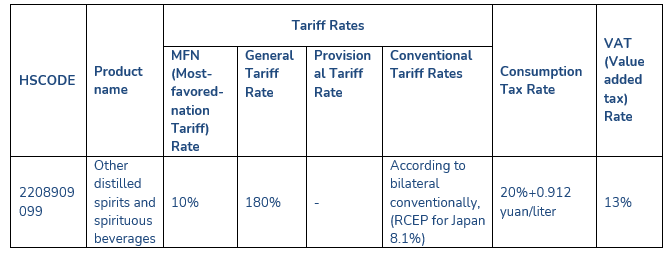

According to the reference big data, Chuhai is a cocktail made from distilled spirits, soda water, and fruit flavorings. According to Chapter 22 of the "Explanatory Notes to the Customs Tariff of Import and Export" [5], the goods are highly likely to be classified under 2208909099.

Source: The above tax rates are sourced from the official website of the General Administration of Customs (GACC) [6] as of April 17, 2025.

Table 2. Different tax rates for Chuhai from the official website of the General Administration of Customs (GACC) [6]

For example: Assuming that the country is Japan which is a most-favored nation and a member of RCEP, and the quantity of its imported Chuhai is 1000 liters. The Dutiable Value (CIF) is 2700 yuan.

Tariff = Dutiable Value * Tariff Rate

= 2700 * 8.1%

= 218.70 yuan (Based on value: MFN (Most-favored nation tariff) rate of 10%. Conventional Tariff Rates RCEP Japan 8.1% applying the lower rate 8.1%; If there are other conventional tariff rates in the future, the lower applicable rate should be used.)

Consumption Tax = [(Dutiable Value + Tariff) / (1 - Consumption Tax Rate)] * Consumption Tax Rate + Quantity of Goods * Unit Consumption Tax Rate Amount

= [(2700 + 218.7) / (1 - 20%)] * 20% + 1000 liters * 0.912 yuan/liter

= 1641.675 yuan (collected as 1641.68 yuan) (Based on value and quantity per Table 2)

VAT = (Dutiable Value + Tariff + Consumption Tax) * VAT rate

= (2700 + 218.7 + 1641.68) * 13%

= 592.8494 yuan (collected as 592.85 yuan)

Total taxes = Tariff + Consumption Tax + VAT

= 218.70 + 1641.68 + 592.85

= 2453.23 yuan

2.3 Whisky, Around 45% Alcohol

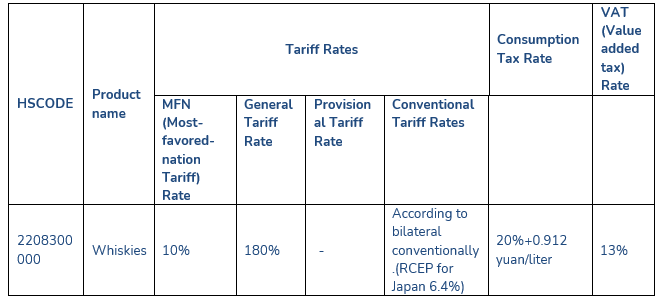

According to Chapter 22 of the "Explanatory Notes to the Customs Tariff of Import and Export" [5], the goods are highly likely to be classified under 2208300000.

In 2025, for whisky, the provisional tariff rate of 5% has been canceled.

Source: The above tax rates are sourced from the official website of the General Administration of Customs (GACC) [6] as of April 17, 2025.

Table 3. Different tax rates for Whisky from the official website of the General Administration of Customs (GACC)[6]

For example: Assuming that the country is Japan which is a most-favored nation and a member of RCEP, and the quantity of its imported whisky is 1000 liters. The Dutiable Value (CIF) is 2700 yuan.

Tariff = Dutiable Value * Tariff Rate

=2700 * 6.4%

= 172.80 yuan (Based on value: MFN (Most-favored nation tariff) rate of 10%, provisional tariff rate of - (or none, because it got canceled in 2025), Conventional Tariff Rates RCEP Japan 6.4% applying the lower rate 6.4%; If there are other conventional tariff rates in the future, the lower applicable rate should be used.)

Consumption Tax = [(Dutiable Value + Tariff) / (1 - Consumption Tax Rate)] * Consumption Tax Rate+Quantity of Goods * Unit Consumption Tax Rate Amount

= [(2700 + 172.80) / (1 - 20%)] * 20% + 1000 liters * 0.912 yuan/liter

= 1630.20 yuan (Based on value and quantity)

VAT = (Dutiable Value + Tariff + Consumption Tax) * VAT rate

= (2700 + 172.80 + 1630.20) * 13%

= 585.39 yuan

Total taxes = Tariff+ Consumption Tax+ VAT

=172.80 + 1630.20 + 585.39

= 2388.89 yuan

Conclusion

- In China, imported goods are required to declare customs duties which include taxes to be paid to clear customs.

- China applies a formula to calculate the total taxes including tariffs to be paid for imported goods.

- There are different types of tariff rates for imported goods in China and are subject to the product and the country of origin.

- In countries and regions that have signed trade agreements with China, conventional tariff rates or preferential tariff rates and provisional tariff rates can be applicable for imported alcoholic beverages. In all cases, whichever the lowest tariff rate should be applied to calculate the tax.

- There is a consumption tax for all imported and local alcoholic beverages in China, and the tax is relatively high.

- Therefore, the total taxes calculated for imported alcoholic beverages as illustrated above are high.

- In 2025: 1) The tax rate for Beer will remain unchanged. 2) The tax rate for Ready-to-drink beverages will decrease due to the RCEP reduction from 8.6% to 8.1%. 3) The tax rate for Whisky will increase due to the cancellation of the provisional tariff rate of 5%, despite the RCEP tax rate decreasing from 7.3% to 6.4%.

3. References

1. Customs Law

http://www.customs.gov.cn//customs/302249/302266/302267/356575/index.html

2. Administrative Measures for the Levy of Import and Export Duties

http://www.customs.gov.cn/customs/302249/zfxxgk/hggzk/6177117/index.html

3. Provisional Regulations on Consumption Tax of the People's Republic of China

https://flk.npc.gov.cn/detail2.html?ZmY4MDgwODE2ZjNjYmIzYzAxNmY0MTFhZWZmOTE3NjQ

4. Tariff law (in force as of December 1, 2024, replacing the Regulations of Import and Export Customs Duties)

https://www.gov.cn/yaowen/liebiao/202404/content_6947843.htm

5. Explanatory Notes to the Customs Tariff of Import and Export

http://www.customs.gov.cn/customs/302427/302442/jckszspjpmzscx/index.html

6. Official website of the General Administration of Customs (GACC)

http://online.customs.gov.cn/ociswebserver/pages/jckspsl/index.html

7. Customs (of a region) [L indicates Most Favored Nation]

https://www.singlewindow.cn/#/parameterDetail?pqcode=CusCountry

8. Free Trade Agreement and Preferential Trade Arrangement Implemented Tariff Table Indicates countries or regions with Conventional Tariff Rates and Preferential Tariff Rates 2025

https://www.gov.cn/zhengce/zhengceku/202412/P020241228532881981193.pdf

https://www.gov.cn/zhengce/zhengceku/202412/content_6995067.htm

Was this article helpful?