Tax Policy on Alcohol

- 5 Mins to read

- DarkLight

Tax Policy on Alcohol

- 5 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Philippines

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 18 Feb 2025 | 22 Feb 2025 | N/A (new report) |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol Goods

Excise tax collection in the Republic of the Philippines is collected from goods that are harmful to people’s health such as alcoholic beverages, tobacco, or luxury goods (decorations, jewels, and perfumes) including goods that destroy the environment or businesses that have concessions such as automobile, mineral and petroleum including oil. [1]

In reference to Republic Act 10351 [2] and BIR Revenue Regulations No. 2-97 [3], these are the classification of excisable alcohol products:

- Distilled spirits - refer to liquors produced from products such as coconut, cassava, nipa sap, camote, buri palm or from fruit juice, syrup, or sugar cane, including whisky, brandy, rum, vodka, gin, and other similar products or mixtures. It is the substance known as ethyl alcohol, ethanol, or spirits of wine, including all dilutions, purifications, and mixtures thereof, from whatever source, by whatever process produced.

- Wines - refer to fermented liquors that have undergone fermentation (no distillation) from fruit juice or anything from fruits, including sparkling wines, champagnes, still wines, and fortified wines.

- Fermented Liquors - refer to beer, lager beer, ale, porter, and other fermented liquors, except tuba, basi, tapuy, and similar domestic fermented liquors.

Persons liable to Excise Tax:

- Manufacturer or producer of locally manufactured or produced alcohol products;

- For imported alcohol products, the excise tax shall be paid by the importer or owner.

Excise Tax is a tax on the production, sale, or consumption of a commodity in a country. It applies to goods manufactured or produced in the Philippines for domestic sale or consumption or for any other disposition; and to imported goods.

Excise Tax Collection Agencies:

- Bureau of Internal Revenue (BIR)

- Bureau of Customs (BOC)

The BIR is responsible for the collection of all internal revenue taxes, fees, and charges through the enforcement of tax laws. The function of the BOC is to manage the collection of excise tax from imported goods. [1]

2. Specific Requirements on Tax Policy per Product

In reference to BIR Excise Tax Rates [4] and BIR Form 2200-A Excise Tax Return for Alcohol Products [5], below are the applicable tax rates. Effective 1st January 2025, the specific tax rate shall be increased by 6% every year thereafter.

Specific Tax refers to the excise tax imposed based on weight or volume capacity or any other physical unit of measurement; Ad Valorem Tax refers to the excise tax imposed based on the selling price or other specified value of the goods/articles. [4]

The manner of computation shall be based on the following: Specific Tax = Weight/Volume/other physical unit of measurement x Specific Tax Rate Ad Valorem Tax = Volume X Selling Price or any specified value per volume x Ad Valorem Tax Rate.

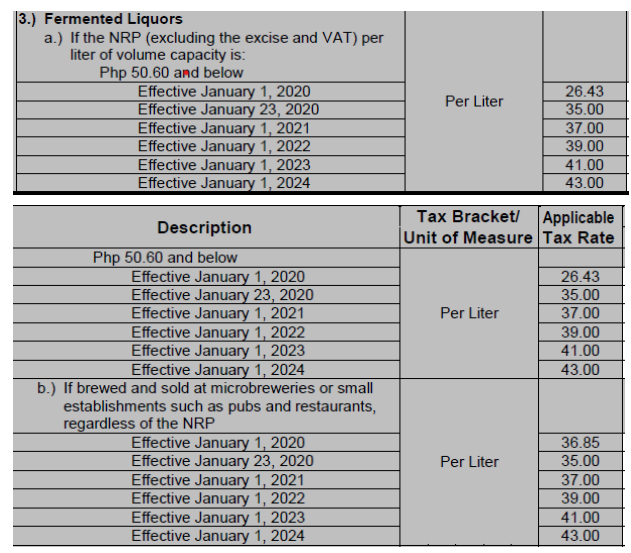

2.1 Beer

The tax rate currency is in ₱ (peso). NRP refers to Net Retail Price.

The tax rate currency is in ₱ (peso). NRP refers to Net Retail Price.

2.2 Ready-to-drink beverages (mainly Chuhai*)

The tax rate currency is in ₱ (peso).

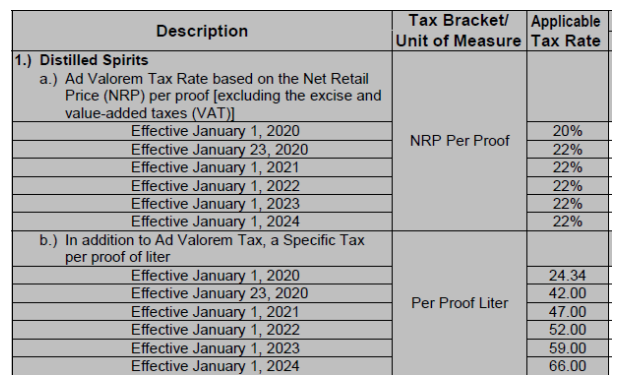

2.3 Whisky

Same as above. Refer to Section 2.2 Tax Rates.

3. Additional Information

Penalties

There shall be imposed and collected as part of the tax:

- A surcharge of twenty-five percent (25%) for the following violations:

- Failure to file any return and pay the amount of tax or installment due on or before the due date; or

- Filing a return with a person or office other than those with whom it is required to be filed unless otherwise authorized by the Commissioner; or

- Failure to pay the full or part of the amount of tax shown on the return required to be filed, or the full amount of tax due for which no return is required to be filed on or before the due date; or

- Failure to pay the deficiency tax within the time prescribed for its payment in the notice of assessment.

- A surcharge of fifty percent (50%) of the tax or of the deficiency tax, in case any payment has been made before the discovery of the falsity or fraud, for each of the following violations:

- Willful neglect to file the return within the period prescribed by the Code or by rules and regulations; or

- A false or fraudulent return is willfully made.

- Interest at the rate of double the legal interest rate for loans or forbearance of any money in the absence of an express stipulation as set by the Bangko Sentral ng Pilipinas from the date prescribed for payment until the amount is fully paid: Provided, That, in no case shall the deficiency and the delinquency interest prescribed under Section 249 Subsections (B) and (C) of the National Internal Revenue Code, as amended, be imposed simultaneously.

- Compromise penalty as provided under applicable rules and regulations [5].

Conclusion

- In the Philippines, excise tax is collected from alcohol products by BIR and BOC.

- For imported alcohol products, excise tax is paid by the importer or owner.

- Classification of alcohol products are Distilled Spirits, Wines, and Fermented Liquors.

- Excise tax rates effective 1st of January 2024

- Beer – Php 43 per liter (specific tax)

- Ready-to-drink beverages (mainly Chuhai) and Whisky – Php 66 per liter (specific tax) and 22% (ad valorem tax rate)

3. References

1. Philippines Excise Department

https://webdev.excise.go.th/aec-law/en/excise-en-philippines.php#:~:text=There%20are%20two%20state%20agencies,and%20the%20Bureau%20of%20Customs

2. Republic Act 10351 [refer to pdf]

https://elibrary.judiciary.gov.ph/thebookshelf/showdocsfriendly/2/51245

3. BIR REVENUE REGULATIONS NO. 2-97 [refer to pdf]

https://elibrary.judiciary.gov.ph/thebookshelf/showdocs/11/46992

4 Bureau of Internal Revenue_Excise Tax

https://www.bir.gov.ph/excise-tax

5. BIR Form 2200-A Excise Tax Return for Alcohol Products

https://bir-cdn.bir.gov.ph/local/pdf/2200-A%20Jan%202020%20ENCS%20Final%20version2.pdf

Was this article helpful?