Tax Policy on Alcohol

- 2 Mins to read

- DarkLight

Tax Policy on Alcohol

- 2 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Taiwan

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 08 July 2024 | 09 July 2024 | N/A (new report) |

| V1 | 17 May 2025 | 19 June 2025 | Overall review and update (e.g. Amendment of the "Tobacco and Alcohol Tax Act" in Jan 2025). |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol

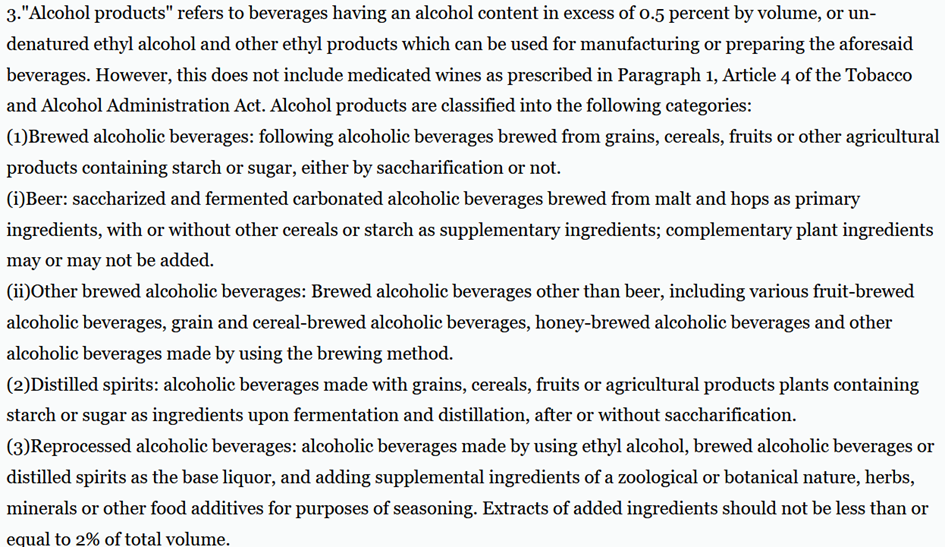

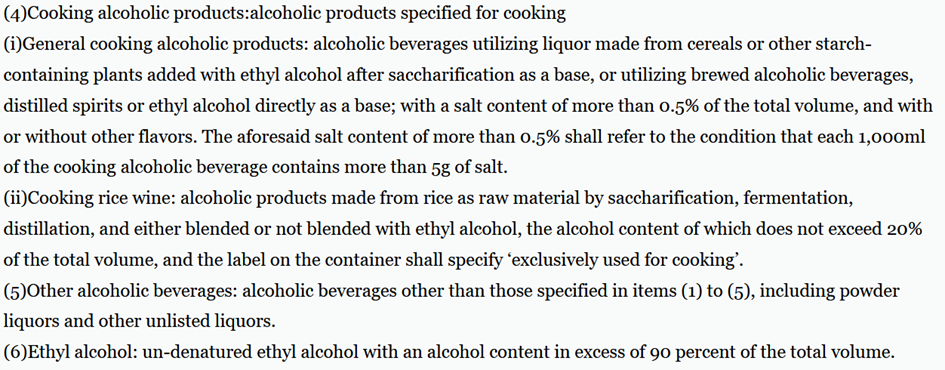

Tobacco and Alcohol Tax Act [1] lays down requirements for alcohol products. Alcohol products are defined in Article 2 as:

2. Specific Requirements per Product

Articles 3 and 4 of the Tobacco and Alcohol Tax Act [1] define the taxes for alcohol products imported from abroad. Upon importation, the tax shall be paid to the Custom by the receiver of the products, holder of the bill of lading, or the holder of the goods.

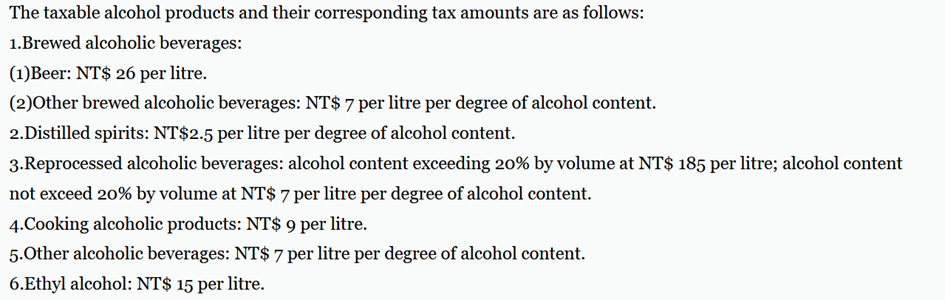

Article 8 provides the tax amount for various types of alcohol products:

In particular,

- Beer is subject to NT$ 26 per liter.

- Alcohol Ready-to-drink beverages/Chuhai fall under “Other alcoholic beverages” subject to NT$7 per liter per degree of alcohol content.

- Whisky, around 45% alcohol falls under “Distilled spirits" subject to NT$2.5 per liter per degree of alcohol content.

Conclusion

- In Taiwan, all alcohol products, regardless of the type of alcoholic beverage and if locally manufactured or imported, are required to pay tax according to the Tobacco and Alcohol Tax Act.

- The same act provides the tax amount for each type of alcohol product.

- Beer is subject to NT$ 26 per liter, Ready-to-drink beverages (mainly Chuhai) to NT$ 7 per liter per degree of alcohol content, and Whisky (distilled spirit) to NT$2.5 per liter per degree of alcohol content.

3. References

1. Tobacco and Alcohol Tax Act – amended 2025-01-24

Was this article helpful?