Tax Policy on Alcohol

- 8 Mins to read

- DarkLight

Tax Policy on Alcohol

- 8 Mins to read

- DarkLight

Article summary

Did you find this summary helpful?

Thank you for your feedback

Tax Policy on Alcohol

Australia

The below version control table serves to document all updates made to the report. The purpose is to ensure the information is always accurate and up-to-date.

| Version Number | Content Creation Date | Publishing Date | Section(s) Updated & Reason(s) for Update |

|---|---|---|---|

| V0 | 2 July 2024 | 4 July 2024 | N/A (new report) |

| V1 | 7 May 2025 | 5 June 2025 | Overall update (including the latest ATO Excise Duty rates for alcohol) and insights for 2025 (e.g. a new proposal to apply GST on dried or dehydrated fruits that are designed for flavoring or decorating alcoholic beverages). |

Disclaimers

A) At RegASK, we are committed to providing our clients with the most up-to-date and accurate information on regulatory requirements and compliance. To ensure the highest level of accuracy and relevance, we regularly review and update our e-guidebooks at least twice per year to reflect the latest regulatory developments in the market. (Please contact us if you wish to activate this feature.) In the meantime, our RegAlerts service is designed to keep our clients notified of any regulatory updates that may impact their business.

B) The contents on this platform are exclusively intended for the use of RegASK and its authorized representatives. All materials herein are confidential and the sole property of RegASK. Any reproduction, distribution, or display of this content to others is strictly prohibited without the express written consent of RegASK.

1. General Requirements on Tax Policy for Alcohol

Australia’s tax system includes monies collected at the Federal, state/territory, and local council levels. The taxes most relevant to alcohol are:

- Goods and Services Tax (GST)

- Indirect taxes (including customs and Excise duties, and licensing)

Goods and Services Tax (GST)

GST is a broad-based tax of ten percent on most goods and services sold in Australia. As a value-added tax, GST is levied on the value added at each stage of a product's production and distribution. While it is levied on most transactions in the production process, GST is usually refunded to most parties in the chain other than the final consumer. The GST rules are complicated, with income collected being directly distributed to the states and territories. This is managed by the Australian Taxation Office (ATO) [1].

Some products are exempt, including:

- Most basic foods (fruit and vegetables, some infant foods, tea, and coffee unless sold ready-to-drink, eggs, fats and oils, flour, sugar, most bread, and many more)

- Bottled drinking water with no additives

- Sales through duty-free shops

- Exports if conditions are met

A full list of exempted goods is available on the ATO website [2]. There is also a searchable online list [3] that clarifies GST status and conditions for many food and beverage products. The online list includes all changes made up to 28 August 2024, which reflect changes due to the Australian GST system following the May 2024 Australian Budget. In relation to alcoholic beverages, the following apply (Table 1):

Note that any changes to the GST list due to the 2025 Budget (delivered on 25 March 2025) are not yet available. Changes to the online list will be available later in the year once the impacts on GST are examined and the searchable online list [3] will be updated once this occurs.

Item | GST status | Notes |

Beer | taxable | Applies to non-alcoholic, light, and normal beer |

Wine | taxable | Includes non-alcoholic wine and wine-making ingredients |

Spirits, including whisky | taxable |

|

Liqueurs | taxable |

|

Alcoholic pre-mixed drink |

| For example, rum and cola (in a can) |

Table 1: examples of GST status extracted from ref [3]

While there were no proposed GST changes specifically relating to alcoholic beverages in the 2025 Australian Budget, there is currently a review for dried or dehydrated fruit for addition to beverages [4]. The ATO has identified that dried or dehydrated fruits that are designed for flavoring, or decorating alcoholic beverages, are taxable because they are ingredients for beverages and are not GST-free under the GST Act. The current entry for ‘fruit (fresh, dried, canned, packaged)' as GST-free will continue to apply until this matter is reviewed [4]. No expected date has been provided for this.

GST applies to items used to package, label, and transport alcoholic beverages within Australia. These would include containers and closures, labels, outer cartons, and shippers, and all transport and store facility fees as relevant. Businesses within Australia using these items and services are usually able to claim back the GST they have paid. GST also applies to product imports.

Imports

GST is payable on imported goods unless the goods are covered by an exemption. Exemptions include those permitted under the GST Act [5]. For ease of review, these exemptions have been collated on the Australian Border Force (ABF) website [6]. The other exemption for GST is specified Customs duty concession items such as the Wine Equalization Tax Exemptions [7], which are also listed in [6]. None of the exemptions apply to imports of alcoholic beverages manufactured overseas and destined for wholesale or retail sale in Australia. Therefore, GST is payable on these products. The GST is usually paid at the same time as any customs duty.

The ABF is responsible for checking the GST exemptions claimed by importers are correct and the value of the taxable importation is correctly calculated. The amount of GST is ten percent of the value of the taxable importation which is the sum of [6]:

- the customs value (CV) of the imported goods,

- any Duty payable,

- the amount paid or payable to transport the goods to Australia and to insure the goods for that transport (T&I), and

- any Wine Equalization Tax (WET) payable, if applicable.

Other charges, which vary, are required for clearance, warehousing, and administrative charges [8]. It is recommended that the client engages an experienced customer broker or import specialist experienced in the importation of alcoholic beverages.

Duty and Excise Tax

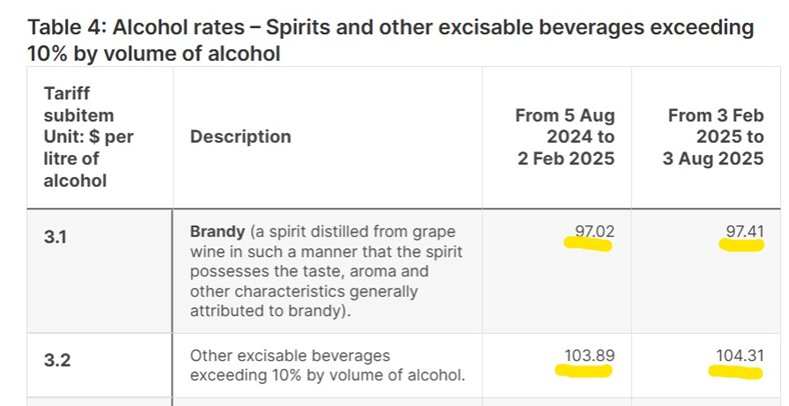

The import Duty is based on the type of alcoholic beverage being imported (e.g., wine, beer, or spirits) and the percentage of alcohol in the beverage. For beers and spirits, there are generally only two main costs involved (Duty and GST). Alcohol is subject to excise equivalent Duty which is equivalent to the excise tax rates applied by the ATO [9]. Rates are updated twice a year in line with the upward movement of the Consumer Price Index (CPI). A copy of the current rate tables (January 2025) is provided [9]. The next planned increase is on 4 August 2025.

Spirits exceeding ten percent alcohol by volume currently have a rate (per liter of alcohol) of AU $97.41 for brandy and AU $104.31 for other spirits, including whisky (Figure 1). Information on other alcoholic beverages is included in the provided copy of [9].

Figure 1: Current excise rates per liter of alcohol (to next increase in August 2025) from ref [9]

Licenses for Excisable alcohol

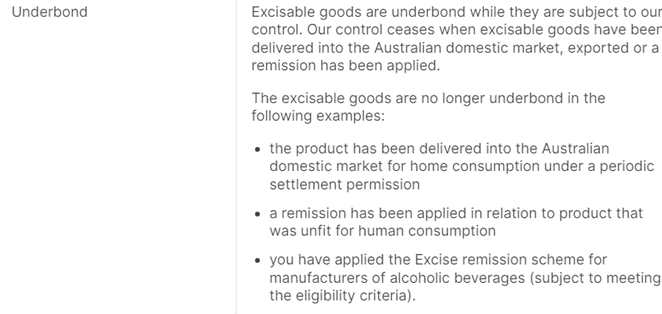

Australian businesses that manufacture, produce, or store ‘underbond’ alcohol products (definition of ‘underbond’ in Figure 2 from ref [10]) require an excise license. There are different types of excise licenses for particular situations [11] and these are administered by the Australian Taxation Office (ATO). The license types are for:

- Manufacturer license

- Storage license

- License to brew on-premises

- Duty-free license

Overseas manufacturers do not require an excise license to send alcoholic beverages to Australia. Packaging isn’t considered a manufacturing process for excise purposes. However, blending spirits or adding flavors or colors to them does require a license.

Figure 2: Definition of ‘underbond’ from ref [10]

There is no application or renewal fee for an excise license. In some cases, a bond is charged to cover some of the expected excise which will ensure that these are collected by the ATO. Other information, including conditions of licenses and administrative functions, is included on the ATO website [9,10,11].

In summary, alcohol in Australia is controlled by different taxes:

- Goods and services tax (GST): applied at multiple points, and at retail sale

- Excise: applied at import and also ongoing for domestic licensed businesses

- Customs charges

A major shortcoming of the tax policy is that the mix of tax measures results in the tax payable by consumers for a ‘standard drink’ (a serve that contains 10 grams of pure alcohol) differs across the types of alcoholic beverages. This is mostly due to the difference between the application of WET (for wines, based on the financial value of beverages) and Excise (based on the percentage of alcohol in a beverage). Figure 3 below illustrates this well. Industry association, Spirits and Cocktails Australia [12] has highlighted the financial and compliance burdens experienced by its membership due to the biannual review of the Excise tax applied per liter of product.

Figure 3: Cost of tax per standard drink across alcoholic beverage types from ref [12]

2. Specific Requirements per Product (Whisky, around 45% Alcohol)

Whisky and other spirits are taxed domestically under the Excise tax (refer to Figure 1) which is based on a charge per liter of alcohol in a product. The scale differs between products with less than ten percent alcohol and more than ten percent. Whisky is also subject to GST (10%). For importation, import duty, customs, GST, other fees and charges may apply.

3. Other Rules

In addition to Australian-based Licences for Excisable alcohol from the ATO (Federal government), there are various state, territory, and local government requirements for licensing of domestic premises and other regulatory aspects such as dangerous goods storage and transportation.

Conclusion

- In Australia, tax policy covering alcoholic beverages is multi-faceted and is inconsistent between different types of products. Beer and spirits (including whisky) are subject to the Excise tax which is based on the volume of alcohol contained in the product. Whisky above 10% alcohol is currently AU $ 104.31 per liter in tax.

- Customs duties that apply to most alcoholic beverages are based on both the percentage of alcohol and the monetary values of the products.

- GST (10%) applies across many facets of commercial alcoholic beverage transactions, including import, transport, packaging, and shipping materials on top of ongoing excises and taxes.

- A major shortcoming of the tax policy is that the mix of tax measures means that the tax payable by consumers for a ‘standard drink’ (a serve that contains 10 grams of pure alcohol) varies depending upon beverage type (Figure 3). The tax on whisky and other spirits is a lot higher than that for beer and wine.

- A new proposal, which is still being considered by the ATO, is to apply GST on dried or dehydrated fruits that are designed for flavoring, or decorating alcoholic beverages. Currently, these would be exempt under the case for ‘fruit (fresh, dried, canned, packaged)', No timeline has been provided for the proposed change.

4. References

1. Australian Taxation Office (ATO) GST information page

https://www.ato.gov.au/businesses-and-organisations/gst-excise-and-indirect-taxes/gst/how-gst-works

2. List of GST-exempt foods from the ATO website

3. ATO full list of foods with GST status (searchable)

https://www.ato.gov.au/law/view/document?DocID=GII%2FGSTIIFL1%2FNAT%2FATO%2F00001&document=document

4. Australian Taxation Office (ATO) webpage ‘Emerging GST issues for food and beverage products'

5. A New Tax System (Goods and Services Tax) Act 1999

https://www.legislation.gov.au/C2004A00446/latest/downloads

6. Australian Border Force page on GST exemptions

7. Wine equalisation tax (WET)

8. Australian Border Force page on Duties and other charges for imports

9. ATO Excise Duty rates for alcohol

(PDF of current rates attached below)

10. ATO Alcohol excise key terms webpage

11. ATO Alcohol excise licensing webpage

12. Spirits and Cocktails Australia webpage - The case for reviewing spirits excise settings

https://www.spiritsandcocktailsaustralia.com.au/advocating-for-a-fair-and-sustainable-spirits-tax/

Was this article helpful?